Why a gold standard is a very bad idea

“Far from being synonymous with stability, the gold standard itself was the principal threat to financial stability and economic prosperity between the wars.” Barry Eichengreen, Golden Fetters.

The extraordinary monetary easing engineered by central banks in the aftermath of the 2007-09 financial crisis has fueled criticism of discretionary policy that has taken two forms. The first calls for the Federal Reserve to develop a policy rule and to assess policy relative to a specified reference rule. The second aims for a return to the gold standard (see here and here) to promote price and financial stability. We wrote about policy rules recently. In this post, we explain why a restoration of the gold standard is a profoundly bad idea.

Let’s start with the key conceptual issues. In his 2012 lecture Origins and Mission of the Federal Reserve, then-Federal Reserve Board Chair Ben Bernanke identifies four fundamental problems with the gold standard:

- When the central bank fixes the dollar price of gold, rather than the price of goods we consume, fluctuations in the dollar price of goods replace fluctuations in the market price of gold.

- Since prices are tied to the amount of money in the economy, which is linked to the supply of gold, inflation depends on the rate that gold is mined.

- When the gold standard is used at home and abroad, it is an exchange rate policy in which international transactions must be settled in gold.

- Digging gold out of one hole in the ground (a mine) to put it into another hole in the ground (a vault) wastes resources.

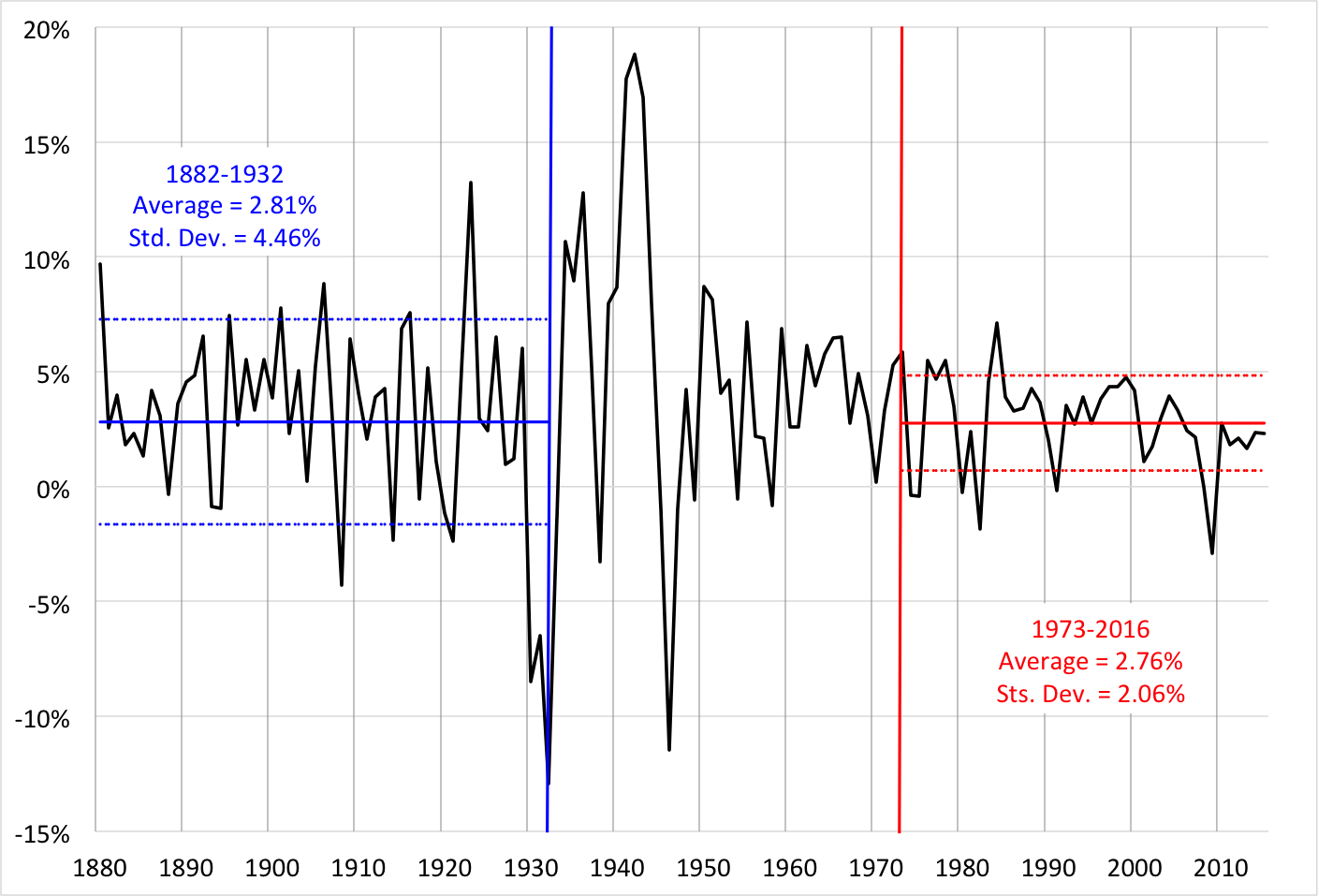

Consistent with Bernanke’s critique, the evidence shows that both inflation and economic growth were quite volatile under the gold standard. The following chart plots annual U.S. consumer price inflation from 1880, the beginning of the post-Civil War gold standard, to 2015. The vertical blue line marks 1933, the end of the gold standard in the United States. The standard deviation of inflation during the 53 years of the gold standard is nearly twice what it has been since the collapse of the Bretton Woods system in 1973 (denoted in the chart by the vertical red line). That is, even if we include the Great Inflation of the 1970s, inflation over the past 43 years has been more stable than it was under the gold standard. Focusing on the most recent quarter century, the interval when central banks have focused most intently on price stability, then the standard deviation of inflation is less than one-fifth of what it was during the gold standard epoch.

Annual Consumer Price Inflation, 1880 to 2016

Source: Federal Reserve Bank of Minneapolis.

What about economic growth? Again, the gold standard was associated with greater volatility, not less. The following chart plots annual growth as measured by gross national product (gross domestic product only came into common use in the 1991.) The pattern looks quite a bit like that of inflation: the standard deviation of economic growth during the gold-standard era was more than twice that of the period since 1973. And, despite the Great Recession, the past quarter century has been even more stable. To use another, simpler, measure, in the period from 1880 to 1933 there were 15 business cycles identified by the National Bureau of Economic Research. That is, on average there was a recession once every 3½ years. By contrast, since 1972, there have been 7 recessions; one every 6 years.

Annual GNP Growth, 1880-2016

Source: FRED and Romer (1986).

Finally, consider a crude measure of financial stability: the frequency of banking crises. From 1880 to 1933, there were at least 5 full-fledged banking panics: 1893, 1907, 1930, 1931, and 1933. Including the savings and loan crisis of the 1980s, in the past half century, there have been two.

So, on every score, the gold standard period was less stable. Prices were less stable; growth was less stable; and the financial system was less stable. Why?

We see six major reasons. First, the gold standard is procyclical. When the economy booms, inflation typically rises. In the absence of a central bank to force the nominal interest rate up, the real interest rate falls, providing a further impetus to activity. In contrast, countercyclical monetary policy—whether based on a Taylor rule or not—would lean against the boom.

Second, the gold standard has exchange rate implications. While we do not know for sure, we suspect that current U.S. advocates of a shift to gold are thinking of the case where the United States acts alone (rather than waiting to coordinate a global return to the gold standard). If so, the change would impose unnecessary risks on exporters and importers, their employees and their creditors. To see why, consider the consequences of a move in the global price of gold measured in some other currency, say British pounds. If the pound price of gold changed, but the dollar price of gold did not, the result would be a move in the real dollar-pound exchange rate. That is, unless the dollar prices of U.S. goods and the dollar wages of U.S. workers adjust instantly to offset gold price fluctuations, the real dollar exchange rate changes. In either case, the result would almost surely induce volatility of production, employment, and the debt burden.

More broadly, a gold standard suffers from some of the same problems as any fixed-exchange rate system. Not only can’t the exchange rate adjust to buffer external shocks, but the commitment invites speculative attacks because it lacks time consistency. Under a gold standard, the scale of the central bank’s liabilities—currency plus reserves—is determined by the gold it has in its vault. Imagine that, as a consequence of an extended downturn, people come to fear a currency devaluation. That is, they worry that the central bank will raise the dollar price of gold. In such a circumstance, it will be natural for investors to take their dollars to the central bank and exchange them for gold. The doubts that motivate such a run can be self-fulfilling: once the central bank starts to lose gold reserves, it can quickly be compelled to raise its dollar price, or to suspend redemption entirely. This is what happened in 1931 to the Bank of England, when it was driven off the gold standard. It happened again in 1992 (albeit with foreign currency reserves rather than gold) when Britain was compelled to abandon its fixed exchange rate.

Third, as historians have emphasized, the gold standard helped spread the Great Depression from the United States to the rest of the world. The gold standard was a global arrangement that formed the basis for a virtually universal fixed-exchange rate regime in which international transactions were settled in gold. This meant that a country with an external deficit—one whose imports exceed its exports—was required to pay the difference by transferring gold to countries with external surpluses. The loss of gold forced the deficit country’s central bank to shrink its balance sheet, reducing the quantity of money and credit in the economy, and driving domestic prices down. Put differently, under a gold standard, countries running external deficits face deflationary pressure. A surplus country’s central bank faced no such pressure, as it could choose whether to convert higher gold stocks into money or not. Put another way, a central bank can have too little gold, but it can never have too much.

This policy asymmetry helped transmit financial shocks in the United States abroad. By the late 1920s, the major economies had restored the pre-World War I gold standard. At the time, both the United States and France were running external surpluses, absorbing the world’s gold into their central bank vaults. But, instead of allowing the gold inflows to expand the quantity of money in their financial systems, authorities in both countries tightened monetary policy to resist booming asset prices and other signs of overheating. The result was catastrophic, compelling deficit countries with gold outflows to tighten their monetary policies even more. As the quantity of money available worldwide shrank, so did the price level, adding to the real burden of debt, and prompting defaults and bank failures virtually around the world.

As Liaquat Ahamed puts it in his masterful book about inter-war monetary policy, The Lords of Finance, it was as if the Great Depression was caused by the fact that there was too much gold piled on one side of the giant vault underneath the Federal Reserve Bank of New York (where the bulk of the world’s monetary gold was stored at the time). That is, if only people could have found a way to shift the gold from one country to another, the depression of the 1930s would not have been so great.

Fourth, economists blame the gold standard for sustaining and deepening the Great Depression. What makes this view most compelling is the fact that the sooner a country left the gold standard and regained discretionary control of its monetary policy, the faster it recovered. The contrast between Sweden and France is striking. Sweden left gold in 1931, and by 1936 its industrial production was 14 percent higher than its 1929 level. France waited until 1936 to leave, at which point its industrial production was fully 26 percent below the level just 7 years earlier (see here and here.) Similarly, when the U.S. suspended gold convertibility in March 1933—allowing the dollar to depreciate substantially—the financial and economic impact was immediate: deflation turned to inflation, lowering the real interest rate, boosting asset prices, and triggering one of the most powerful U.S. cyclical upturns (see, for example, Romer).

Turning to financial stability, the gold standard limits one of the most powerful tools for halting bank panics: the central bank’s authority to act as lender of last resort. It was the absence of this function during the Panic of 1907 that was the primary impetus for the creation of the Federal Reserve System. Yet, under a gold standard, the availability of gold limits the scope for expanding central bank liabilities. Thus, had the Fed been on a strict gold standard in the fall of 2008—when Lehman failed—the constraint on its ability to lend could again have led to a collapse of the financial system and a second Great Depression.

Finally, because the supply of gold is finite, the quantity available to the central bank likely will grow more slowly than the real economy. As a result, over long periods—say, a decade or more—we would expect deflation. While (in theory) labor, debt and other contracts can be arranged so that the economy will adjust smoothly to steady, long-term deflation, recent experience (including that with negative nominal interest rates) makes us skeptical.

This brings us back to where we started. Under a gold standard, inflation, growth and the financial system are all less stable. There are more recessions, larger swings in consumer prices and more banking crises. When things go wrong in one part of the world, the distress will be transmitted more quickly and completely to others. In short, re-creating a gold standard would be a colossal mistake.