Thoughts on Proposed Corporate Tax Reform

“We teach our students that […] the benefits of a simpler, more easily administered tax system that treats different forms of income more equally may well rise as our need for revenue rises. We also teach them that progressive taxation involves a trade-off between equity and efficiency and that, when revenue requirements rise, the efficiency cost of redistribution rises as well.” Alan J. Auerbach, The Future of Fundamental Tax Reform, 1997.

With a Republican government intent on major changes in fiscal policy, it’s useful to start thinking about the fundamentals of taxing and spending. The analysis below focuses narrowly on the House-proposed tax reform (pages 24-29) for large firms – what is commonly known as the corporate tax.

Let’s start with a few general points regarding objectives and methods. Our primary goal here is to consider how to raise revenues efficiently, not how to spend or distribute them. So, whatever one might believe regarding the desirable scale of the government safety net or the supply of public goods, that is beyond our immediate focus. Instead we ask how to minimize the negative impact of taxes on economic growth for a given revenue target.

Two principles are usually associated with efficient taxation. The first is to impose the lowest tax rate consistent with raising the required revenue. The second, to impose the tax as broadly and evenly as possible across all goods and services.

Setting a low tax rate on a broad tax base limits the impact on incentives to work, save, invest, and produce, reducing distortions that weaken long-run growth. That is, such a strategy minimizes the “deadweight” loss from taxation—the income that is lost by all parties (consumer, producer and government) due to distorted incentives. And, since goods produced tomorrow are different from those produced today, the second principle implies that the tax rate should be steady over time.

Beyond our focus on efficiency, we also consider the distributional impact of a tax. However, to the extent that distributive goals can be achieved by adjusting spending, this matters less. Moreover, the true burden of a tax, the incidence, can be difficult to measure and it is generally unrelated to the way the tax is collected. For example, in a small, open economy with free cross-border flow of capital, the required after-tax rate of return on investment is the world rate. Consequently, local taxes on capital are not borne by the owners of the capital used in production. Instead, the burden of the tax is passed on to those purchasing the output and to domestic labor.

Finally, because most taxes distort behavior, assessing any specific tax raises the question “compared to what”? In considering tax reform proposals, since the revenue must come from somewhere, you are stuck comparing one set of distortions with another set.

Regarding corporate taxation, a simple non-differentiated tax on profit should exhibit no difference between the marginal and average tax rates. In contrast, the loopholes and exemptions in the existing corporate tax promote tax avoidance and lead to a large, persistent gap between the top marginal corporate tax rate and the average effective tax rate (measured as a share of aggregate corporate profits; see chart). For the period since 1952, that “efficiency gap” was at its narrowest just after the last major tax reform of 1986, and has re-widened substantially. This pattern suggests that there is a case for reforming the corporate tax.

United States: Top corporate tax rate and the average effective tax rate, 1947-2017

Note: The average effective tax rate is the ratio of revenues from the corporate tax to aggregate corporate profits in the national accounts. Sources: FRED and (for the top corporate tax rate) Tax Policy Center.

The House proposal is to replace the existing tax on corporate profits with a destination-based cash flow tax (DBCFT). In addition to lowering the tax rate from the current 35% to 20%, the DBCFT has three key features:

- It removes the deductibility of interest payments.

- It excludes investment from the tax base.

- It imposes a border adjustment (taxing imports at the full rate and exempting exports).

So long as it does not lower revenue, the new tax imposes a lower, less differentiated, tax rate on a broader base. This is clearly consistent with greater efficiency.

Let’s consider the three changes one-by-one.

Interest deductibility. Currently, firms may deduct net interest payments from the profits on which corporate taxes are assessed. However, they may not deduct equity dividends or buybacks. By removing the deductibility of interest, the reform would eliminate the differential tax treatment of debt and equity for corporations. While mitigated by aspects of personal income taxation, the existing bias in the corporate tax promotes borrowing, adding to the risks in the financial system.

At this writing, it is not at all clear how the proposed changes will handle financial intermediaries. That is, what will happen to institutions that have net interest income? Our hope is that the reforms will treat bank interest expenses in a manner that discourages leverage in the same way that it does for nonfinancial corporations. (For a discussion of the impact of the corporate tax on bank leverage, see this recent IMF cross-country study.)

Investment exclusion. By excluding investment from taxation, the reform converts the corporation tax from a tax on profit to a tax on cash flow (profit minus investment). In contrast to complex depreciation rules that currently set the pace at which investments may be deducted from a firm’s tax base, a cash flow tax treats depreciation as instantaneous. Imposing a zero marginal tax on all new investment favors long-lived assets. While this constitutes a distortion, it probably offsets other distortions in the tax code that favor short-lived assets (such as the lack of inflation adjustment for capital gains) or that favor residential over business capital (such as the mortgage interest deduction). As an indication of greater efficiency, the investment exclusion would help reduce the large existing variation in the marginal effective tax rates across categories of firm investment, ranging from equipment and structures to intellectual property (see Table 8 here).

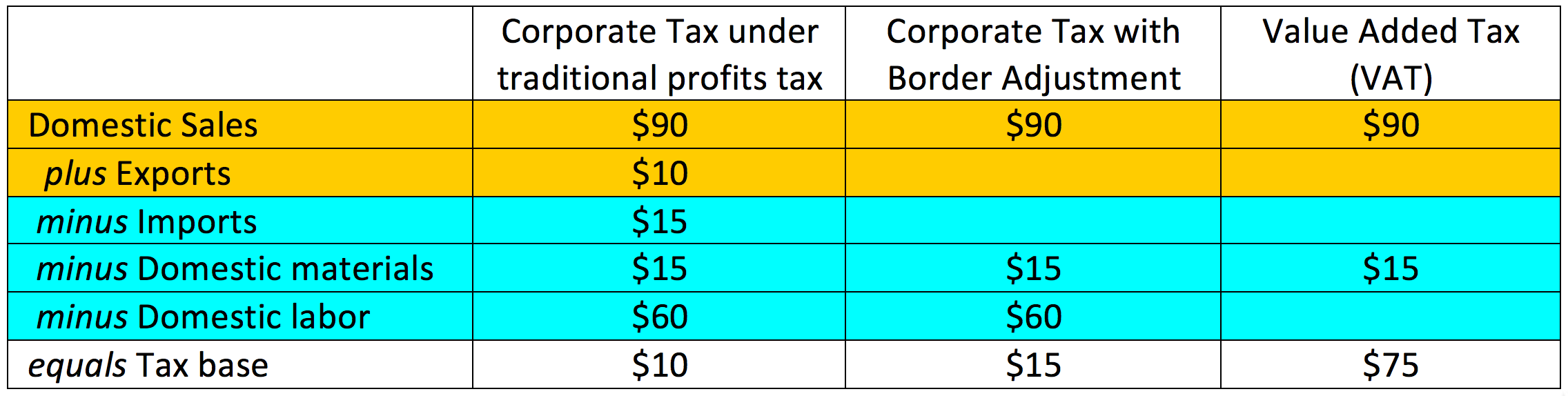

Border adjustment. Allowing a firm to deduct exports from its tax base, but disallowing a deduction for imports, converts the corporate tax from one that is production-based to one that is destination-based. This exclusion of cross-border transactions from the tax base is the most complex of the three changes. To help understand it, start with a simple example of how to calculate the tax base for a firm with and without a border adjustment. For a firm with gross income equal to $100 ($90 from domestic sales and $10 from exports) that spends $90 on inputs ($15 on imports, $15 on domestic materials, and $60 on domestic labor), the tax base under a traditional corporate profits tax with no border adjustment is equal to $10. That is, $90+$10-$15-$15-$60 = $10 (see table). With the border adjustment, the tax base would rise to $90-$15-$60 = $15.

Firm tax base under different tax structures

Note: Items shaded in yellow are the firm’s revenues; those shaded in blue are its expenditures. For complex examples, including border adjustments that turn the tax base negative, see Auerbach and Holtz-Eakin (2016).

A value-added tax (VAT) includes such a border adjustment, which is permitted under World Trade Organization (WTO) rules for indirect taxes on consumption (as opposed to direct taxes on income). To the extent that a single VAT rate is applied evenly across goods and services and over time, it minimizes distortions and is widely viewed as efficient. Not coincidentally, countries that have large social insurance programs also typically impose VATs, allowing them to limit the negative impact on economic growth of financing a relatively large public sector. Indeed, objections in the United States to a VAT have often come from opponents of government expansion (see, for example, here). Others may view a VAT as regressive because, at the low end of the income distribution, the consumption taxed constitutes a larger share of income.

A DBCFT is similar to a VAT, so it is not without irony that some who favor a smaller public sector are now advocates, while others who prefer a larger one tend to be opposed. However, a DBCFT is not economically identical to a VAT. Importantly, as the table above shows, the border-adjusted corporate tax excludes domestic labor costs from the tax base, while the VAT does not. In this sense, a border-adjusted corporate tax functions like a VAT plus a reduced tax on domestic labor, making domestic goods and services relatively more competitive.

One attraction of the border adjustment is that it would reduce (if not eliminate) the incentive for firms to find means to shift profits to low-tax foreign venues. For example, in the table above, if the firm lowered its export price to a foreign subsidiary by 50%, lowering exports to $5, its tax base under the traditional profits tax would also fall to $5. In the presence of border adjustments, however, the tax base would not change.

Would a border-adjusted corporate tax comply with WTO rules against discriminatory export subsidies and import taxes? In theory, the competitiveness benefits of border adjustment can be offset by a currency appreciation. And, as Auerbach and Holtz-Eakin argue, given that both VATs and taxes on domestic labor are permitted, it seems odd to view an economically equivalent combination of the two as noncompliant. However, since the DBCFT is a direct tax, that economic assessment need not be decisive for WTO tax lawyers. Were a WTO complaint eventually to succeed, U.S. exporters could face large countervailing duties.

Unsurprisingly, given the scale of the change, the replacement of the corporate profit tax with a DBCFT would result in winners and losers, who are actively lobbying legislators. The former includes exporters with big capital outlays. The key losers are large importers who spend little on plant and equipment.

So, would the proposed 20% DBCFT raise as much revenue as the current 35% corporate tax? Maybe not. The current tax generated about $450 billion in revenue over the year to September, or just over one-fifth of federal tax receipts. The Tax Policy Center estimates that, over the 10 years to 2026, the proposed tax changes (together with others for smaller firms) would lower receipts by an average of nearly $90 billion annually, with that shortfall declining to less than $20 billion annually over the succeeding decade (see Table 2 here).

To be sure, these estimates do not account for the dynamic benefits of a more efficient tax that promotes investment. However, it also remains to be seen how much of the proposed reform will survive the lobbying frenzy. Were key parts of the DBCFT to be omitted from the final tax package—especially the controversial border adjustment—either the shortfall would be much larger or the cut in the tax rate would have to be much smaller.

And what about fairness? If the tax change were revenue-neutral, would a DBCFT alter the distributional impact of the corporate tax? With imports accounting for about one tenth of personal consumption expenditures, a 20% tax could result in a VAT-like one-off increase of more than 2½% in the U.S. price level. However, we expect that some mix of dollar appreciation and compression of corporate margins will at least partly offset this impact. Dollar appreciation also would diminish the U.S. net foreign asset position.

Broadly speaking, the larger the price increase (the smaller the exchange rate appreciation), the more regressive the likely tax incidence relative to the existing tax. With respect to the net foreign asset position, Farhi, Gopinath and Itskhoki estimate that a 20% appreciation of the dollar—in response to a 20% DBCFT—would result in a capital loss of about $2½ trillion, or about 2.9% of wealth. However, given the unequal distribution of wealth, this outcome is consistent with the view that the larger the currency appreciation, the less regressive the incidence of the tax.

Rather than focus on this uncertain mix of currency appreciation, higher prices and loss of wealth, we believe greater attention should be paid to the relative efficiency of the DBCFT compared to the existing corporate tax. In our view, all three elements of the new tax proposal—the elimination of interest deductibility, the deductibility of investment, and the border adjustment—would improve on what is currently a very inefficient corporate tax system.

To be sure, as with many taxes, there is probably a trade-off: the increase in efficiency may be accompanied by a decline of fairness (see our earlier post). But, other aspects of the House tax proposals—especially those that cut top personal income tax rates—may be far more regressive than the DBCFT. And, we expect that taxes will need to rise in the future to finance a larger public sector. If so, tax efficiency will be all the more important, just as Alan Auerbach argued 20 years ago.