Ending Too Big to Fail

“We very, very much did not want to make the loan.” Ben Bernanke testimony (October 10, 2014) regarding the Federal Reserve’s emergency provision of credit to AIG in September, 2008.

More than six years after the Dodd-Frank Act passed in July 2010, the controversy over how to end “too big to fail” (TBTF) remains a key focus of financial reform. Indeed, TBTF—which led to the troubling bailouts of financial behemoths in the crisis of 2007-2009—is still one of the biggest challenges in reducing the probability and severity of financial crises. By focusing on the largest, most complex, most interconnected financial intermediaries, Dodd-Frank gave officials a range of crisis prevention and management tools. These include the power to designate specific firms as systemically important financial institutions (SIFIs), a broadening of Fed supervision, the authority to impose stress tests and living wills, and (with the FDIC’s “Orderly Liquidation Authority”) the ability to facilitate the resolution of a troubled SIFI. But, while Dodd-Frank has likely made the U.S. financial system safer than it was, it does not go far enough in reducing the risk of financial crises or in ensuring credibility of the resolution mechanism (see our earlier commentary here, here and here). It also is exceedingly complex.

Against this background, we welcome the work of the Federal Reserve Bank of Minneapolis and their recently announced Minneapolis Plan to End Too Big to Fail (the Plan). While the Plan raises issues that require further consideration—including the potential for regulatory arbitrage and the calibration of the tools on which it relies—it is straightforward, based on sound principles, and focuses on cost-effective tools. In this sense, the Plan represents a big step forward.

The TBTF problem is fairly simple. It comes down to this: facing the looming failure of a SIFI, a government can be expected to bail out the private institution’s creditors rather than allow the country to suffer an economic and financial collapse. The historical record is littered with examples of such bailouts. The 2007-09 experience, when U.S. regulators (both Republicans and Democrats) did this repeatedly, is just the most recent example, and one that we should never forget.

Simply declaring TBTF illegal and forbidding government bailouts may be popular, but it lacks credibility. TBTF is a classic problem of time consistency: a future government facing a crisis will always renege on the promise not to bail out private creditors. If necessary, it will simply change the law, as the U.S. Congress did when it approved the $700-billion Troubled Asset Relief Program in September 2008. As a result, today’s SIFIs and their creditors have a clear incentive to take risks that raise the chances of a financial crisis. As a result, they are too leveraged and undertake excessive transformation of liquidity, maturity, and credit.

What to do? The answer is that we need a regulatory framework that severely reduces the probability of a crisis as well as the potential contagion from the resolution of troubled intermediaries. This may mean trading off financial safety for economic efficiency. But, as we have discussed in an earlier post, the social costs seem likely to be lower than many argue. The necessary changes will also be highly unpopular among the regulated intermediaries who will be called on to sacrifice their private profit opportunities in order to reduce the potential for socially costly negative spillovers to the financial system as a whole.

A key virtue of the Minneapolis Plan is its realistic assumptions. The first is that SIFIs (designated or not) will be bailed out in a crisis; the second, that making the financial system safe will involve some up-front costs. It also assumes that, fearing contagion and regardless of claims that bank debts are going to be bailed-in, a future government will be unwilling to impose losses on SIFI creditors during a period of widespread financial distress. (Again, the experience from the 2007-2009 crisis proves the point.) Implicitly, the Plan also assumes that regulators are not capable of anticipating all of the key vulnerabilities of the financial system, so that preventing future crises requires making the financial system resilient to all possible types of large shocks, even those we can’t imagine. Finally, the Plan requires that the benefits of any regulatory regime must exceed the costs. Accordingly, it does not try to eliminate financial crises, but instead aims to reduce their frequency to an acceptably low level (specifically, once in 100 years).

So, what are the key features of the Plan? There are four:

- A sharp increase in requirements for loss-absorbing equity capital (not debt) at the 13 largest, most complex, and most interconnected banks (currently those with at least $250 billion in assets) to be phased in over five years.

- A further sharp hike in capital requirements after five years for each bank unless the Treasury Secretary certifies that it is no longer systemically important.

- A tax on borrowings by shadow banks (based on the types of shadow banks defined by the Financial Stability Board) calibrated to match the increased funding costs of the “covered bank” group (with a higher tax rate on shadow banks that the Treasury Secretary considers systemic).

- A relaxation of regulation on banks with up to $10 billion in assets. (These account for 98 percent of FDIC-insured banks, but less than 19% of the insured deposit base nationwide.)

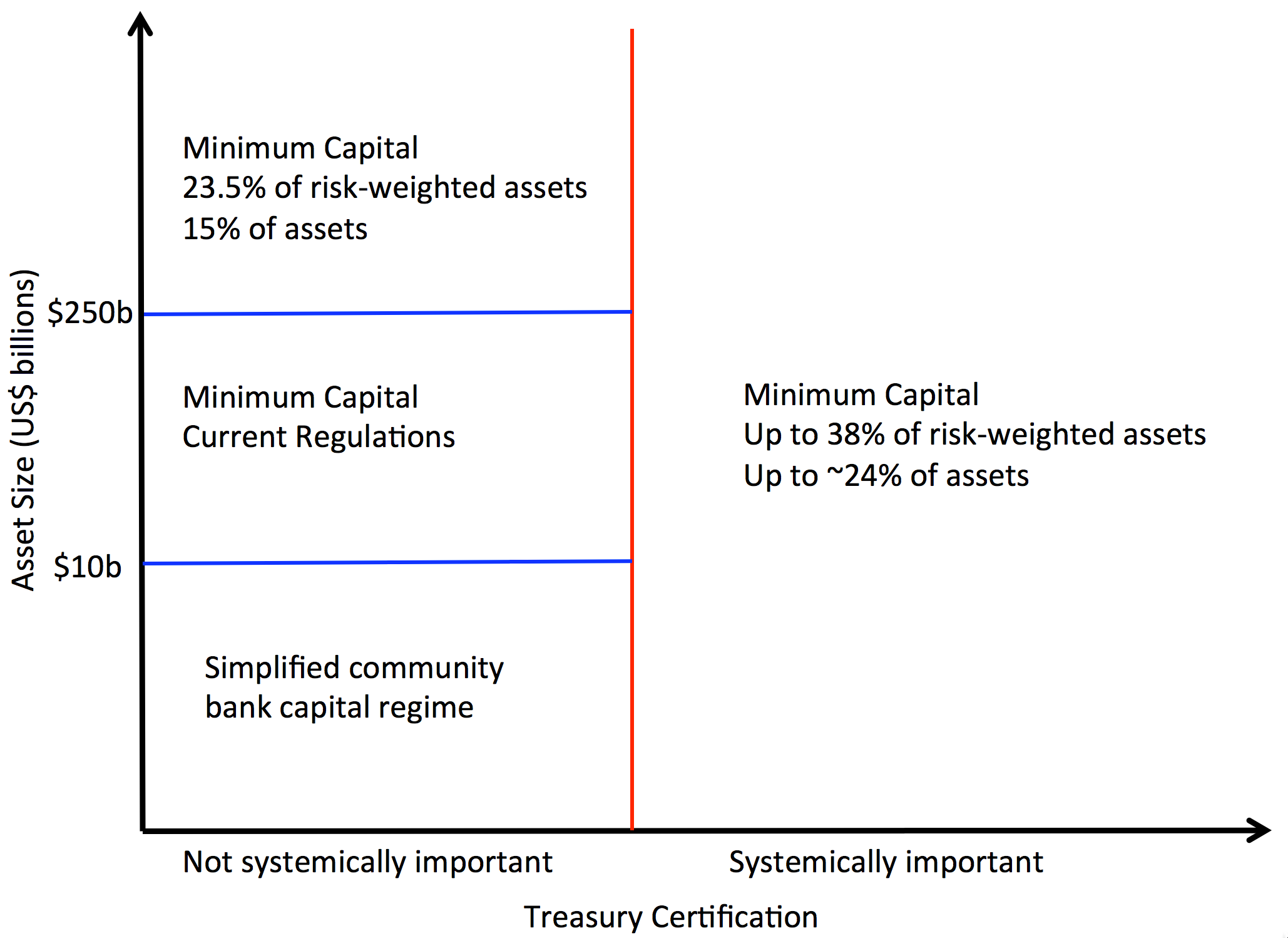

The following chart illuminates the Plan’s impact on the banking sector. Following a five-year transition, covered banks will need to finance 23.5% of their risk-weighted assets (RWA) with equity (formally Common Equity Tier 1—CET1—consistent with Basel III reforms and the Dodd-Frank Act). This 23.5% level matches the Fed’s Total Loss Absorbing Capital (TLAC) requirement for SIFIs. But, while TLAC includes long-term debt (see our earlier posts here and here), the Minneapolis Plan excludes debt instruments under the realistic assumption that authorities will bail out all bondholders in a crisis.

Based on end-2015 covered bank reporting, the Plan translates the 23.5% RWA requirement into a pure leverage requirement (the ratio of common equity to total assets) of 15%. (For comparison, the FDIC’s mid-2016 Global Capital Index reports that the average Tier 1 capital ratio of the 8 U.S. “G-SIBs”—Global Systemically Important Banks—equals 13.55% of RWA and, under GAAP accounting, 8.24% of total assets). Moreover, after five years, unless the Treasury Secretary certifies that a covered bank is no longer systemic, its required capital ratio would rise by 5 percentage points per year to a peak of 38% of risk-weighted assets (equivalent to an unweighted leverage ratio of nearly 24%). Finally, banks with assets fewer than $250 billion and more than $10 billion would continue to face capital requirements as they are currently structured, while those banks with fewer than $10 billion in assets would face simpler, less stringent requirements.

Minneapolis Plan: Capital Regime for Bank

Source: FRB Minneapolis, The Minneapolis Plan to End Too Big to Fail, Figure 1 and the authors.

The tax regime for shadow banks is simpler than the capital requirements (see following chart). The universe of institutions covered includes the types of nonbank intermediaries monitored by the Financial Stability Board (see, for example, here). The tax applies to firms with more than $50 billion of assets. There are only two tax rates: 1.2% for firms certified by the Treasury Secretary as not systemic; and 2.2% for the rest. This two-tiered tax is intended to mimic the additional funding cost arising from the two-tiered capital requirements for covered banks. A portion of the shadow-banking tax (an estimated 0.4% according to the Plan) merely offsets the U.S. tax subsidy that permits deduction of interest payments, but not dividends.

Minneapolis Plan: Tax Regime for Shadow Banks

Source: FRB Minneapolis, The Minneapolis Plan to End Too Big to Fail and the authors.

In addition to its realistic assumptions, the Minneapolis Plan has a number of other virtues. The first is its clarity in matching objectives with tools. It relies on equity capital, not only as the surest shock absorber in the financial system, but also as a device to induce large banks to shrink, reduce their complexity, and become less interconnected. An intermediary funding 38 percent of risk-weighted assets (or nearly 24 percent of overall assets) with equity—the long-run default requirement unless the Treasury Secretary declares the bank to no longer be systemic—would have a buffer sufficient to dramatically reduce its chance of failure even under extreme stress.

Second, the Plan anticipates a prime mechanism for its circumvention: namely, the migration of risk from banks to less-regulated shadow banks, some of which already are systemic. It aims to levy the same constraint on the systemic activities of shadow banks that it does on covered banks (see our post here). This follows the macroprudential regulatory principle established by Hanson, Kashyap and Stein: “impose similar capital standards on a given type of credit exposure irrespective of who winds up holding the exposure.” Again, the Plan takes a simple approach: its broad tax on the borrowing of shadow banks is designed to mimic the additional funding cost that higher capital standards impose on a covered bank. Doing so should limit the competitive disadvantage of covered banks and the migration of risk.

Third, unlike some proposals, the Plan acknowledges Dodd-Frank’s continued role in ending TBTF. Dodd-Frank’s stress tests would help verify compliance with capital standards, discourage “covered banks” from loading up on systemic risk, and help identify efforts to conceal risk (say, by shifting it off balance sheet or by using derivatives to create synthetic leverage). Similarly, living wills would still encourage large banks to make themselves simpler and less connected and facilitate their resolution. By accepting these aspects of Dodd-Frank, the Plan treats those covered banks that remain systemic after five years the way utility regulators treat nuclear power plants: “While not risk free, they are so highly regulated that the risks of failure are effectively minimized.”

Fourth, by focusing regulatory attention on the largest, most complex, most interconnected institutions in the financial system—as of midyear, the 8 U.S. G-SIBS alone held assets worth $10.7 trillion accounting for nearly 70% of all commercial bank assets—and by penalizing the most systemic shadow banks through a supplementary tax regime, the Plan would allow regulators to relax the constraints imposed by Dodd-Frank on most financial institutions whose failure imposes no threat to the financial system as a whole. We suspect that the opportunity to ease regulatory requirements would not be limited to banks with fewer than $10 billion of assets. According to one measure of systemic risk—the Stern V-Lab’s SRISK measure—the top 10 banks currently account for more than two thirds of aggregate U.S. SRISK, while only one bank with fewer than $100 billion in deposits makes up even 1% of the total.

Fifth, the Plan exhibits appropriate humility regarding the calibration of its capital requirements and tax rates. We have little idea of exactly where to set these, but society will benefit from learning by doing. Limiting the likelihood of a severe crisis to once in a 100 years requires modeling that probability, along with the banking and economic losses in the event of a crisis. Because severe crises occur infrequently, researchers rely on a cross-country crisis database (see here) and must make numerous assumptions (including, for example, deciding which countries and crises to include in the sample and whether recent institutional changes have altered the likelihood and severity of crises in ways that are not represented in the sample). But humility shouldn’t lead one to shy away from policy reform: the alternative is to accept the status quo, which is probably neither safe enough nor efficient.

Finally, the Plan allocates discretionary power over the financial system where it is most likely to be effective: to the Treasury Secretary. The Secretary can command the resources necessary to judge whether a financial intermediary is systemic and can enforce her decision. In addition to the Treasury’s own Office of Financial Research, the Secretary can call on the various regulatory agencies for information and guidance about the institutions they supervise. Facing less risk of institutional capture than these agencies, the Treasury has the incentive to treat threats to financial stability in the same way regardless of the type of legal entity that creates them. And, in the event that a TBTF intermediary still fails, the Secretary (together with the Federal Reserve) can call on the FDIC to arrange a Dodd-Frank-authorized orderly liquidation. This streamlining of governance is a significant step beyond Dodd-Frank’s reliance on the Financial Stability Oversight Council’s powers to designate SIFIs and to coordinate the efforts of U.S. regulators to address threats to financial stability.

So, where are the weaknesses in the Plan? First, are the thresholds for covered banks ($250 billion of assets) and for assessment of shadow banks ($50 billion of assets) appropriate? Such arbitrary numbers always invite regulatory arbitrage: the Plan provides the Treasury Secretary some leeway in assessing systemic risk for banks below the covered threshold, but it is unclear how effective this would be in practice. Second, the list of shadow banks is open to debate. Which types of institutions should be in and which should be out? At the moment, the Plan excludes insurers, despite evidence that some insurers engage extensively in shadow banking. Finally, how can the tax on shadow banking be implemented so as to minimize circumvention? Our hope is that the public comment process will help answer some of these questions, improving the structure of the Plan.

So, what’s the bottom line? While the Minneapolis Plan needs much further analysis (and probably considerable tinkering with its parameters), the broad design provides a solid basis for legislation that would advance the public goal of making the financial system safe in a cost-effective way. The key is to strengthen the resolve of future policymakers to do what the Federal Reserve could not do in 2008 with AIG—deny emergency credit even in a period of financial distress. By reducing the probability of the politically corrosive bailouts that TBTF engenders, the Plan also would help restore confidence in a critical tenet of capitalism—that risk-takers in the financial system not only profit from success, but also bear the full costs of failure. Absent such confidence, it is entirely possible that the extraordinary benefits of free enterprise and competitive markets will disappear.