Recent Commentary:

Money, Banking, and Financial Markets

Congress mandates the Federal Reserve to achieve maximum sustainable employment and price stability. Artificial intelligence (AI) affects both. The role of Chair Warsh’s Productivity and Jobs Task Force is to help the Federal Open Market Committee (FOMC) understand those effects. Its charge is to “assess the economic impact of new general-purpose technologies, including artificial intelligence, to inform the Federal Reserve's policy judgments.”

So how should the Task Force address this challenge? More to the point, what does the FOMC need to know about AI? The Task Force should start by conceding that nobody can speak with authority about the size or scope of AI's eventual impact on the economy. The Committee's problem — and by extension the Task Force's — is more manageable:

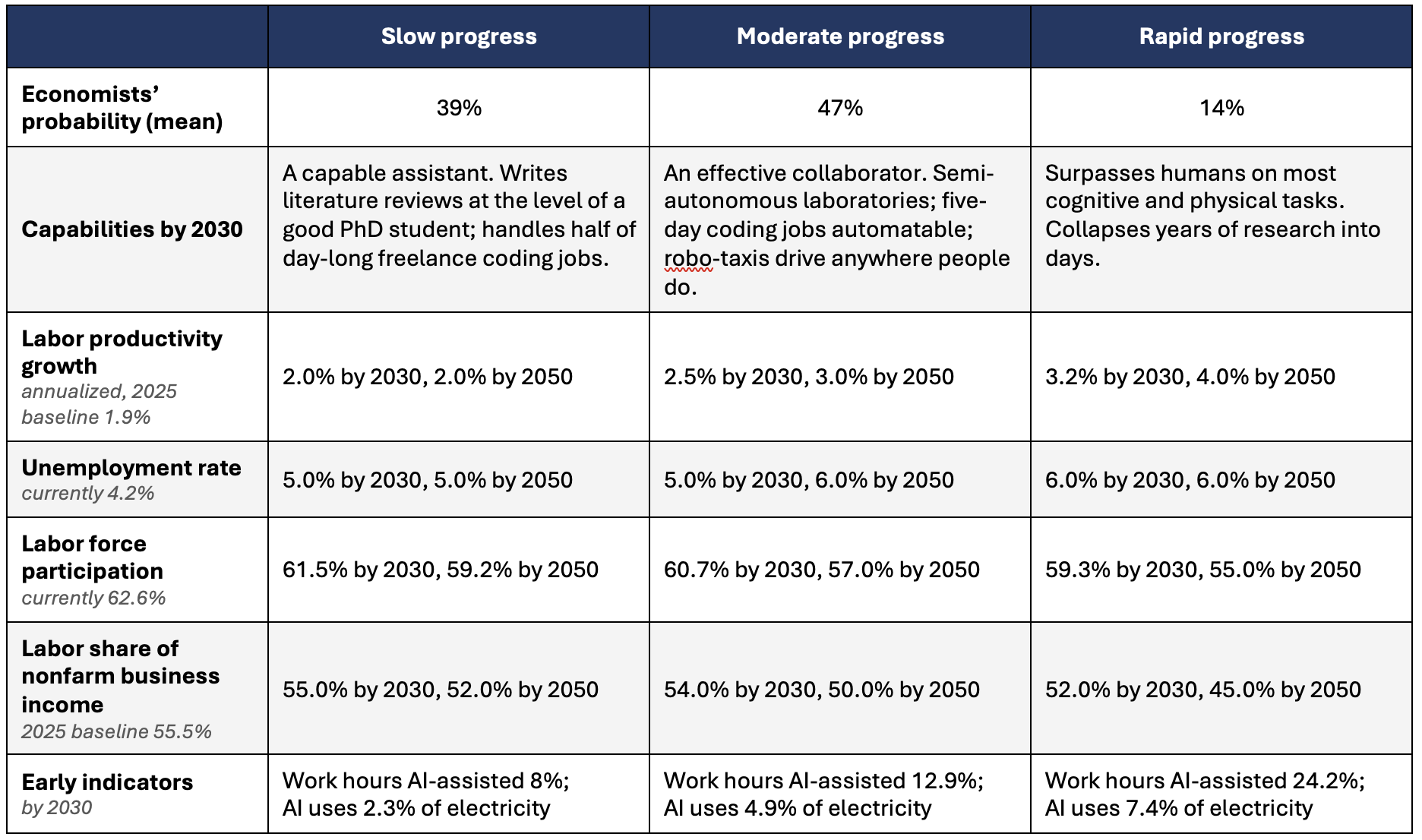

Enumerate a range of plausible paths for the economy.

Identify the indicators that reveal which path we are on.

Establish how much the FOMC can trust its usual policy guides as AI advances.

In what follows, we take a very rough first pass at what the Task Force should do — and, more importantly, of what it should be telling the FOMC to do routinely. We start with three paths the economy might take, built on three Karger et al. scenarios for AI progress by 2030. We ask what evidence would distinguish these paths, how soon that evidence could arrive, and how much the FOMC can rely on the usual unobservable policy benchmarks in the meantime.

We have written seven posts that address Chair Warsh's five task forces. This final post gathers the recommendations in a single place — 22 of them — and notes briefly how they fit together.

Our diagnoses share a common observation. In each of the five areas, the Committee steers by a number nobody observes: the inflation trend, the shock decomposition, the “stars”, the inflection point of reserve demand, and the reaction function itself. The Committee (or the public) infers these, typically using filters calibrated to a past distribution of shocks. Based on some combination of statistical filters and stylized models, these guides become fragile in key episodes, such as the broad pickup of prices in 2021.

The recommendations respond to this unobservables problem in five ways. In some, we ask the Fed to disclose what goes into the numbers it already produces. In others, we urge it to collect what it cannot currently see. In still others, we ask it to design policy that holds up when estimates prove wrong. In another, we urge it to keep checking that its routine estimation methods still work. And in two, we ask it not to discard what it currently produces before a credible replacement is available.