Courting Crisis: The Case Against Cutting Bank Capital Requirements

“The safety and soundness of the banking system is built on trust, and I fear we are eroding that trust.” Federal Reserve Governor Michael S. Barr, Brief Remarks on the Economic Outlook and Monetary Policy, March 26, 2026

We authored this post jointly with our friend and colleague, Professor Jeremy Kress of the University of Michigan Ross School of Business.

On March 19, 2026, the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) issued three notices of proposed rulemaking (NPRs) that would substantially weaken the regulatory capital framework for the largest U.S. banks. The proposals would: (1) revise the Basel III minimum risk-based capital rules for the largest banks; (2) recalibrate the surcharge for global systemically important banks; and (3) update the standardized approach risk-based capital rules.

These proposals are the latest in a sustained campaign to roll back the post-crisis capital framework. They would reduce requirements for common equity tier 1 (CET1) capital — the loss-absorbing cushion of the highest-quality regulatory capital — by nearly $88 billion for the largest and most systemically important institutions. That cut would reduce the system-wide ratio of CET1 capital to risk-weighted assets from 13.4 percent to approximately 12.9 percent.

These cuts come on the heels of other efforts to hollow out the capital framework. Earlier this year, the agencies finalized reductions to the supplementary leverage ratio for the largest banks, justifying that move on the premise that risk-based capital requirements would remain a binding constraint (see our September 2025 comment letter opposing those reductions). The latest proposals run directly counter to that premise. And the dilution of stress tests — another pillar of the post-crisis framework — compounds the effect further. The agencies present each change as modest and self-contained. But together, they represent a severe erosion of the safeguards put in place after 2008.

This post summarizes our forthcoming comment letter to the Federal Reserve, FDIC, and OCC opposing the proposals.

The Post-Crisis Capital Framework

Bank capital — primarily common equity — is the cushion that absorbs losses before a bank becomes insolvent. The more equity financing a bank uses, the more its shareholders stand to lose if things go wrong, and the less likely that taxpayers will be called upon to cover the bill. (For a deeper treatment, see our primer on bank capital and our post on setting capital requirements.)

In the wake of the 2008 financial crisis, the Basel Committee on Banking Supervision — the international body that sets minimum capital standards for the world's major banking systems — developed the Basel III framework, which the United States and other major jurisdictions agreed to implement. That framework applies to internationally active banks and rests on two pillars: risk-based requirements, which link capital to the riskiness of a bank's assets, and the leverage ratio, a simpler measure that requires capital funding to exceed a fixed percentage of total assets regardless of how risky they are. Risk-based requirements are more precise but vulnerable to arbitrage; the leverage ratio is blunt but harder to game. The two pillars reinforce each other because they measure risk differently — which is why watering down either one weakens the whole framework.

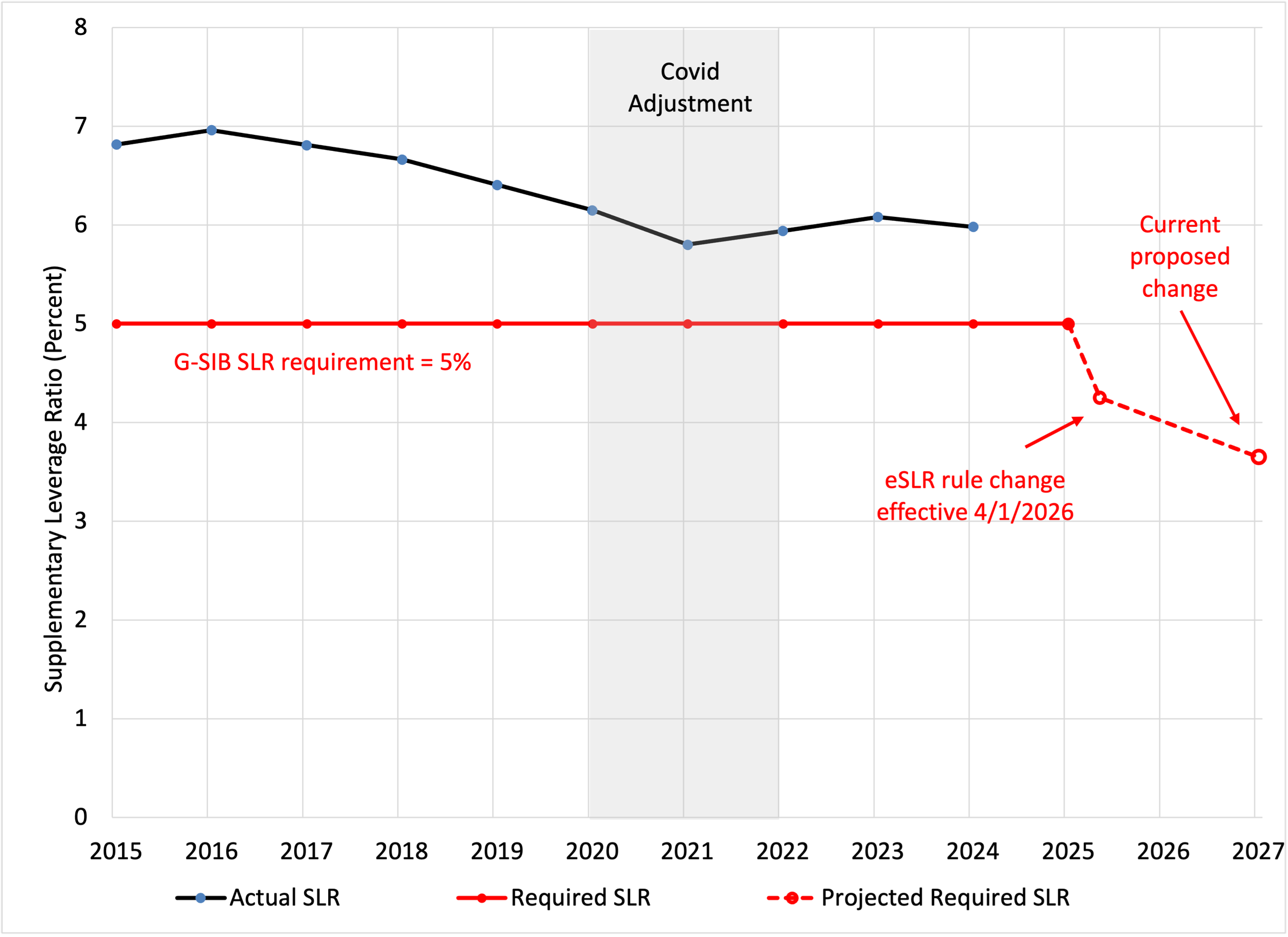

The United States implemented the first phase of the Basel III reforms after the crisis, and for a time the results were encouraging: CET1 risk-weighted ratios rose from low single digits to roughly 13 percent for the largest banks. But Figure 1 tells a more complicated story. The blue line shows the supplementary leverage ratio (SLR), which compares capital with both on- and off-balance-sheet exposures. The United States set the SLR requirement for the U.S. G-SIBs in 2014 at 5 percent — formally, this elevated requirement is called the enhanced SLR (eSLR). The December 2025 rule relaxed this requirement, and the March 2026 NPRs would lower it further. U.S. G-SIBs’ reported SLR peaked at 7 percent in 2016 before falling to about 6 percent — mostly before the COVID policy stimulus.

Figure 1: Leverage Ratio for the Eight Largest U.S. Banks (with projected requirement), 2015–2027P

P Projection. Notes: The blue line shows the actual SLR — capital divided by total leverage exposure (which includes both on- and off-balance-sheet items). All values are exposure-weighted averages for the eight U.S. GSIB bank holding companies. The horizontal red line at 5 percent shows the SLR requirement that applied to all eight GSIBs before April 1, 2026 (formally, the enhanced SLR). The line drops to 3.9 percent on April 1, 2026, the exposure-weighted-average requirement under the December 2025 final rule, which set each GSIB's requirement at 3 percent plus 50 percent of its Method 1 GSIB capital surcharge. The dashed continuation at 3.7 percent shows the projected requirement at the end of 2027 if the March 2026 NPRs are finalized, assuming each GSIB's Method 1 surcharge falls by 50 basis points relative to current levels. Source: Federal Reserve Bank of Kansas City Bank Capital Analysis (Q2 2025 release); Federal Register, December 1, 2025.

The erosion of the SLR reflects banks' choice to expand their balance sheets without commensurate increases in capital — an arbitrage the leverage ratio is designed to prevent. The agencies' current proposals would lower the SLR requirement further, as the dashed red projection suggests. Banks' actual leverage ratios would likely follow, reflecting some mix of payouts to shareholders and increased holdings of assets with relatively low risk weights.

What Are the Proposals, and What Would They Do?

The proposed new rules address three pieces of the capital framework:

The Basel III Proposal would implement (with significant downward deviations) the final Basel III standards for risk-weighted capital. The proposal would allow the largest banks to rely on only one method to calculate their capital requirements. Today, those banks compute risk-weighted assets under both their own internal models and a standardized regulatory approach, meeting capital requirements based on whichever measure is higher. Removing this dual requirement eliminates a key safeguard against model error and gaming.

The G-SIB Surcharge Proposal would reduce the risk-based surcharge that applies exclusively to global systemically important banks (G-SIBs) — the eight largest U.S. bank holding companies, which together account for roughly 60 percent of U.S. banking assets. The proposal runs counter to the aim of this surcharge, which is to make G-SIBs internalize the costs of the systemic risk they impose on the rest of the financial system.

The Standardized Approach Proposal would revise risk weights for credit, equity, and operational risk for a broader range of banks, generally lowering them.

The agencies estimate that their proposals would reduce required capital across the board: by 4.8 percent for the largest banks, 5.2 percent for large regional banks, and 7.8 percent for smaller institutions with less than $100 billion in assets. Most concerning is the $88 billion reduction for the largest banks, whose failure would pose the greatest systemic risk.

The Evidence Does Not Justify the Cuts

The agencies assert that a CET1 ratio of 12.9 percent remains within an "optimal range" — but the academic literature they cite casts doubt on that conclusion. Studies of optimal capital levels yield estimates ranging as high as 31 percent (see here, here, and here), with most credible recent work pointing well above the agencies' target. The agencies cite this research and then ignore it, offering no principled basis for anchoring below the midpoint of a wide range.

The deeper problem with the agencies' analysis is that it is entirely static. The agencies measure the impact of the rule as if banks hold their balance sheets fixed. What actually happens when regulators cut capital requirements? Banks do at least two things. First, they use the reduction to fund dividends and share buybacks. For example, in the first quarter of 2026, in direct response to the agencies’ deregulatory agenda, the largest U.S. banks repurchased a record $33 billion of their own stock. Second, they actively optimize their portfolios in response to changes in requirements — shifting into assets with relatively low risk-weights for a given expected return. As banks arbitrage their risk-based capital ratios, they also typically lower the leverage ratio, potentially until it becomes binding again (see our earlier post).

Finally, there is the question the agencies never squarely address: where is the evidence that lower capital requirements boost lending? U.S. banks substantially increased their capital funding from 2009 to 2016 while simultaneously expanding lending and outperforming their European peers. Better-capitalized banks lend more, especially during stress.

Arbitrarily Cutting the Surcharge for the Largest Banks

Of the $88 billion in aggregate capital reduction for the largest banks, $33 billion flows from revisions to the systemic risk surcharge for the G-SIBs. We have no quarrel with certain technical improvements that the agencies propose, such as using averaged rather than year-end data to reduce incentives to “window dress” at the end of reporting periods or adjusting scoring bands to avoid cliff effects (where a small change in a bank's systemic footprint triggers a large jump in its surcharge). But the proposed recalibration of the surcharge formula is indefensible.

The United States calculates the surcharge using two methods: an international standard shared with other major jurisdictions, and a broader U.S.-specific measure that incorporates additional indicators of systemic risk. The proposal would make a one-time downward adjustment to the U.S.-specific method, ostensibly to eliminate the gap that has opened between the two measures since 2019. As Governor Barr put it in his dissent, this change replaces a principled, risk-based calibration with an arbitrary alignment to the less stringent method. The two approaches measure systemic risk differently by design. There is no analytical basis for expecting them to converge, and no justification for recalibrating the more rigorous one downward simply because it produces higher numbers.

The proposals would also reduce the weight of short-term wholesale funding (STWF) in the surcharge calculation from roughly 30 percent to 20 percent. Since 2016, banks' reliance on STWF has grown from approximately 30 percent to 40 percent of risk-weighted assets. Reducing the weight of the riskiest funding component when banks are accumulating more of it perversely rewards the risk exposure that the surcharge exists to penalize.

Why the “Gold Plating” Argument Is Wrong

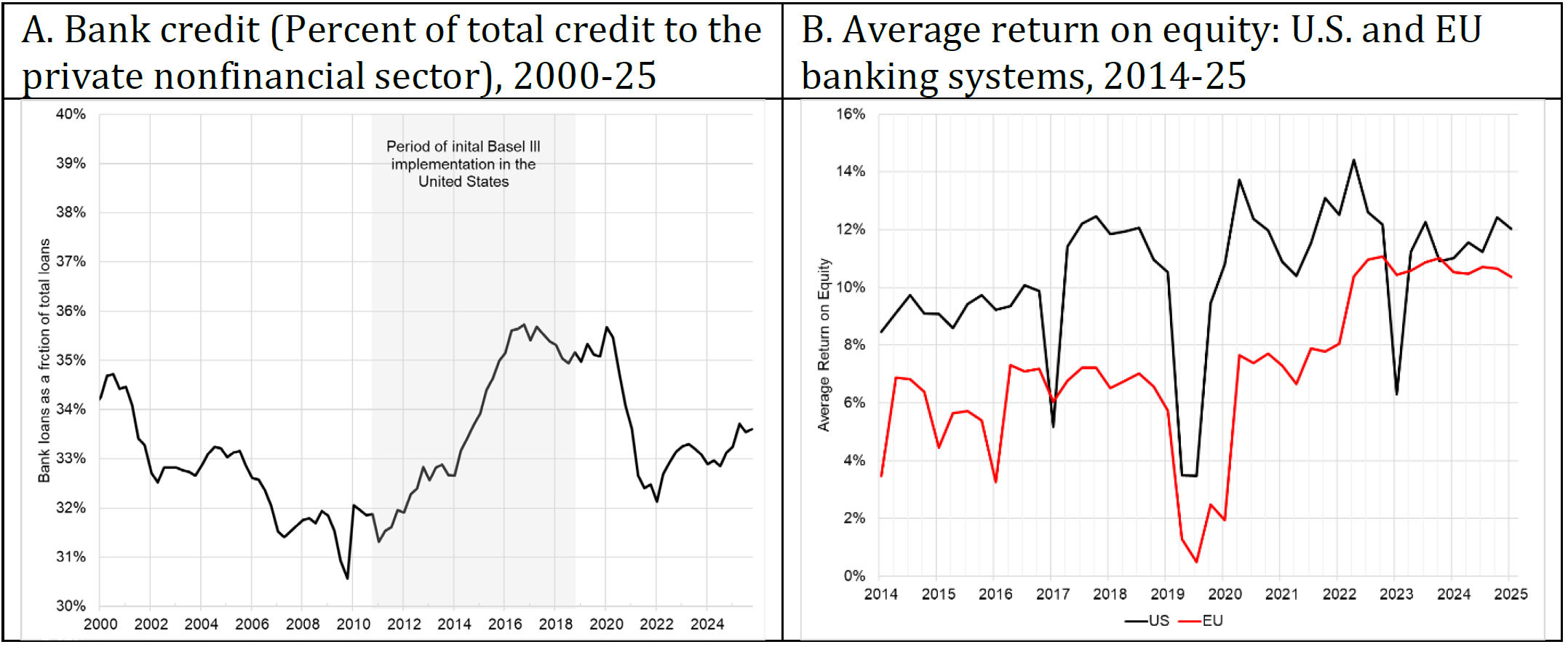

Proponents of the new rules often characterize the existing U.S. framework as "gold plating" — by which they mean that the United States requires more capital than the Basel international minimum. They argue that this approach imposes unnecessary costs on U.S. banks and puts them at a competitive disadvantage. As we explain in our Basel Endgame post, this argument is wrong. As Figure 2 below shows, since at least 2015, well-capitalized U.S. banks have consistently outperformed their European peers, delivering higher returns on equity despite higher capital requirements.

The current proposals go well beyond countering “gold plating.” They contain more than 20 material downward deviations from the Basel III standards the agencies claim to be implementing. Three stand out.

First, the Basel III framework includes an output floor — a requirement that model-based capital cannot fall below a minimum based on the standardized approach. The Basel Committee introduced this floor as one of the cornerstones of its 2017 reforms specifically to prevent banks from exploiting internal models to reduce their capital requirements. The U.S. proposal does not just omit the floor; it inverts it, re-purposing the standardized approach as a cap on market risk capital. If a bank's internal models produce a higher capital requirement than the standardized approach, the bank may use the lower standardized number. This change directly undermines the agreed international framework.

Second, the proposal reduces capital requirements when banks use market risk factors with insufficient price data. The Basel framework requires the opposite: when a risk factor lacks reliable price data so that banks cannot model it with confidence, capital requirements should be higher, not lower. Reducing capital for exposures where risk is harder to measure and easier to obscure creates an incentive for banks to shift risk exposure into areas where data is thin and regulatory scrutiny is weakest.

Third, the proposal extends preferential capital treatment to a broader range of securitizations than Basel III permits. Securitizations allow banks to package loans and sell them to investors, moving risk off their balance sheets. When capital requirements on these structures are too low, banks have less incentive to ensure the underlying loans are sound. They also may retain the securitized products on their balance sheets, concentrating rather than dispersing risk.

All three of these deviations from the Basel framework reduce capital where risks are hardest to see and therefore easiest to exploit. (For more details, see our Journal of Economic Perspectives paper.)

The Industry's Competitiveness Arguments Don't Hold Up

Proponents of the new rules make two further arguments for reducing capital requirements: that high requirements push activity into the unregulated nonbank sector, and that they put U.S. banks at a competitive disadvantage relative to their foreign peers. Neither holds up.

On migration: banks actually gained market share between 2011 and 2016 as U.S. regulators implemented the initial Basel III capital increases. Far from driving activity to nonbanks, higher capital requirements coincided with banks lending more, not less.

The argument also fails to distinguish activity migration that lowers systemic risk from migration that raises it. Shifting risk from systemically important, highly leveraged banks to less-leveraged nonbanks can be socially beneficial, provided those nonbanks are appropriately supervised. The burden of proof should rest with the agencies to demonstrate that any such migration raises aggregate systemic risk.

Even in instances where migration is demonstrably harmful, the correct response would be to extend regulation to those nonbank entities — to widen the regulatory perimeter — not to weaken the rules inside it. The policy goal should always be “same function, same risks, same regulation.”

The competitiveness argument fares no better empirically. U.S. banks have operated profitably at higher capital levels for over a decade, outperforming their European and Asian peers. The evidence does not support the notion that a few hundred basis points of additional required capital undermines U.S. banks’ competitive position.

Figure 2 illustrates both our risk migration and competitiveness points. Panel A shows that banks’ share of credit to the private nonfinancial sector has remained broadly stable since 2000 — and actually rose during the 2011-2016 period as U.S. regulators implemented the initial Basel III capital increases, the opposite of what the migration argument predicts. Panel B shows that U.S. banks have persistently outperformed their European peers on return on equity throughout the post-crisis period, despite higher capital requirements.

Figure 2. Bank Credit and Return on Equity Comparison

Panel A: The gray-shaded band marks the 2013–2019 initial implementation period of Basel III. Sources: Panel A is from the Federal Reserve Z.1 Financial Accounts of the United States tables L.100 and L.101.

Panel B is from the FDIC Quarterly Banking Profile and the European Banking Authority Risk Dashboard.

By deviating materially from the Basel framework it helped design, the United States will give other jurisdictions less incentive to comply — potentially setting off a race to the bottom like the one that preceded the 2008 crisis. The United States has long been the anchor of international regulatory cooperation in banking. These proposals put that role at risk.

Errors of Omission

The proposals fail to address two important vulnerabilities that trace directly to the 2023 bank failures: the link between capital and the liability structure, and a loophole allowing banks to conceal unrealized losses on their securities portfolios.

The 2023 failures of Silicon Valley Bank, Signature Bank, and First Republic demonstrated that capital adequacy and liquidity risk are not separable. Banks with large uninsured deposit franchises and long-duration assets face a dangerous risk: the deposit franchise appears to hedge interest rate risk under normal conditions, but when rates rise sharply and the value of long-duration assets plunges, deposits flee — amplifying rather than cushioning the stress (see our earlier post). Higher capital requirements for such institutions are not excessive — they reflect the elevated systemic risks these entities pose. A bank’s capital requirements should take into account its liquidity risk profile — yet these proposals actually attenuate the link between capital and liquidity by devaluing short-term wholesale financing as a component of the G-SIB surcharge.

The proposals also leave a significant accounting loophole unaddressed. Banks hold securities in one of two accounting buckets. Securities classified as "available for sale" (AFS) are marked to market — unrealized gains and losses flow through to reported equity and regulatory capital. In contrast, securities classified as "held to maturity" (HTM) are carried at historical cost — unrealized losses do not affect regulatory capital.

Silicon Valley Bank exploited this distinction catastrophically. By shifting billions into the HTM bucket, it reported strong regulatory capital ratios even as rising interest rates deeply impaired its economic net worth. The disconnect held until depositors noticed and the bank collapsed. Kim, Kim, and Ryan find that SVB was not alone. They document that banks routinely classify securities as HTM to minimize regulatory capital charges, not because they intend to hold them to maturity. The agencies should address HTM classification directly — reforming its scope, transfer rules, and capital treatment to serve the framework's prudential objectives.

Conclusion: A Troubling Pattern

The agencies’ repeated efforts to roll back post-crisis regulatory standards remind us of the admonition of former Bank of England Deputy Governor Paul Tucker: "The history of bank regulation in the United States is of progressive dilutions of core regulatory requirements over a number of years, leaving the banking system as a whole vulnerable to crisis."

Over the past year, regulators have cut the SLR, diluted stress tests, and reduced the Federal Reserve's supervisory capacity by more than 30 percent. The latest proposals would cut risk-based capital further. It may be possible to rationalize each step individually. But taken together, they leave the financial system meaningfully less resilient than it was two years ago.

As Governor Barr said in recent remarks, banking is built on trust. Capital is the foundation of that trust. When the public, counterparties, and markets observe that the largest banks have less capacity to absorb losses, confidence erodes. Governor Barr put it plainly: "I fear we are eroding that trust." Indeed, our trust has worn thin.

We urge the agencies to reconsider. At a minimum, they should withdraw the arbitrary recalibration of the systemic risk surcharge, stop reducing the weight of short-term wholesale funding in the surcharge calculation, and eliminate the material downward deviations from the Basel III standards — particularly the inversion of the market risk output floor, the treatment of hard-to-model risk factors, and the extension of preferential securitization treatment.

They should also reject the nonbank migration argument as a basis for weakening bank capital standards. And, they should reinstate the requirement that the largest banks compute risk-weighted assets under both their own internal models and the standardized regulatory approach, with the capital requirement determined by whichever is higher.

Finally, they should evaluate all capital-related proposals holistically — considering their combined impact with the recent SLR cuts, stress test changes, and banks' evolving liquidity needs — rather than treating each change in isolation. Before finalizing any rules, they should conduct a comprehensive quantitative assessment of the kind the Basel Committee undertakes for its own major reforms — one that models dynamic bank behavior, interaction effects among simultaneous regulatory changes, and systemic risk under stress. Partial, static modeling is simply not fit for purpose.

Note. The Federal Reserve, FDIC, and OCC are accepting public comments on the three proposals through June 18, 2026. We encourage anyone who cares about the resilience of the U.S. financial system to submit a comment here.