The Fed's Reserve Management Revisited

“[T]he constraint of having sufficient reserve balances to make timely outgoing payments throughout the day without relying on funding from the Fed can suddenly have a high and volatile shadow price, disrupting the Fed’s target of market interest rates. It has been difficult for the Fed to accurately predict the supply of reserves necessary to avoid this outcome.” Darrell Duffie, “The Payment System Puts a Floor on the Fed’s Balance Sheet,” BPEA Conference Draft, March 26-27, 2026

Two months ago, we argued that the Federal Reserve's balance sheet was already near its minimum level determined by demand factors, and that shrinking it significantly would risk heightened interest rate volatility without major changes that would themselves carry costs. We framed the pressure to shrink it — driven in part by Fed Chair nominee Kevin Warsh's stated goal of a significantly smaller Fed footprint — as a "cure potentially worse than the disease."

To be sure, a smaller balance sheet is a worthy goal. It would reduce the Fed's presence in credit markets, limit the fiscal-like character that large-scale asset purchases acquire over time, and preserve dry powder for the next crisis. As we noted in our July 2021 post, central bank balance sheets tend to expand sharply in financial crises and never fully contract — a ratchet that on occasion takes on the character of government finance. The question is not whether to shrink the balance sheet, but how to do so without triggering the very instability the central bank exists to prevent.

Our expectation is that shrinking the Fed’s balance sheet from current levels without undermining financial stability is likely to prove a complex and delicate process that could take years to implement. Since our February post, a policy conference paper by Stanford economist Darrell Duffie (see citation above), together with speeches by Dallas Fed President Lorie Logan and by Fed Governor Stephen Miran — the latter accompanied by a co-authored working paper cataloging specific tools for reducing the balance sheet — have explored the factors influencing banks’ aggregate reserve demand, which is now the key driver of the Fed’s balance sheet scale. These new contributions are more optimistic about reducing reserve demand substantially. However, they have not altered our judgment about the desired sequencing and pace of reserve management reforms.

Importantly, the proposed demand-reducing tools are largely untested at scale in the U.S. financial system. We do not know whether they would work as intended, how large their effects would be, or what unintended consequences they might produce. That uncertainty leads us to counsel caution and care, not confidence, as policymakers consider next steps.

Despite that uncertainty, a consensus about how to proceed may be emerging. Above all, the goal ought not be to return to a world of scarce reserves that could entail unwelcome interest rate fluctuations. Avoiding painful volatility surprises requires that policymakers develop a new framework that shifts banks’ reserve demand inward, allowing supply to remain ample even as the Fed’s balance sheet shrinks. Put differently, moves to significantly lower reserve supply should proceed only after measures are in place to ensure lower reserve demand.

While implementing a new framework could well take several years, this post discusses some reform options that are taking shape. Proponents of balance sheet reduction also tend to overlook a fiscal point worth making explicit at the outset: reducing reserves matched by equal reductions in Fed Treasury holdings does not lower the government's combined interest bill — and may well raise it.

Two Ways to Reduce Reserves

As President Logan explains, there are two ways to lower commercial bank reserves, and hence shrink the Fed’s balance sheet. The first, which Logan favors, is to reduce banks’ demand for reserves, such that they need fewer reserves at a given short-term market rate (the interest rate on reserve balances – IORB). The second is to move up the demand curve: slash supply until reserves carry a significant liquidity premium and market rates rise meaningfully above IORB. (In our earlier post, we illustrated this alternative — a leftward shift in reserve supply — and its risks.)

Duffie describes why the scarce-reserves path is treacherous. In a complex and interconnected system, small simultaneous shocks may cascade: in September 2019, routine Treasury settlements and quarter-end pressures combined to send the secured overnight financing rate (SOFR) 315 basis points above IORB and intraday repo rates up nearly 1,000 — the kind of combination that could easily go undetected until it is too late (see here). Such episodes of market dysfunction generally do not arise from supply-demand imbalances that are visible in advance. They can emerge from any number of sources — sudden price movements in other markets, shifts in collateral flows, unexpected changes in the distribution of reserves across banks — that interact in ways that are difficult to foresee.

The Payment System Is the Binding Constraint

From our perspective, Duffie’s key new analytical contribution — one that we did not consider in our previous post and that appears critical for assessing the policy options ahead— is to show how the interbank payment system (the Fed’s Fedwire Funds and Securities Services) is now the primary driver of banks’ structural reserve demand.

Here is the mechanism. As a result of post-crisis regulatory and supervisory changes, globally important banks must demonstrate self-sufficient liquidity — the ability to meet their needs from their own resources without relying on the Fed. Banks worry that accessing daylight overdrafts, borrowing from the discount window, or utilizing the Standing Repo Facility (SRF) signals an inability to satisfy post-crisis liquidity standards. As a result, big banks aim at the start of each day to have reserves sufficient to cover their gross outgoing Fedwire payments without utilizing any Fed facility.

The contrast with the pre-crisis world is striking. Prior to 2008, the 10 largest banks ran average daily daylight overdrafts of roughly $120 billion. Today, the entire banking system averages under $5 billion, even though Fedwire now processes about $7.3 trillion in payments each day, up by more than 40 percent from before the 2008-09 crisis. This substitution of pre-loaded reserves for intraday central bank credit appears to be the single largest impetus for today’s high structural reserve requirement.

A key consequence of this new reserves-in-advance system is that the timing of bank payments has become receipt-dependent. When reserves are thin, large dealer banks wait for incoming funds before sending payments. While individually rational, this behavior can be collectively destabilizing: Copeland, Duffie and Yang show that delays in payments to the 10 largest repo dealer banks reliably predict spikes in SOFR, so that the SOFR-IORB spread, rather than the effective federal funds rate (EFFR), is the relevant stress indicator. In fact, the EFFR, which mostly reflects lending between Federal Home Loan Banks (FHLBs) and foreign banks in a residual $100-billion-a-day market, typically misses what is happening in the repo market entirely – a market the Office of Financial Research estimates at $12.6 trillion per day on a gross basis.

The Tools for Reducing Reserve Demand

What policy tools could the Fed use to shift the reserve demand curve inward? Here is our assessment of the toolkit, integrating the recent papers and speeches with our own analysis. We lead with the approaches that may hold the most promise for achieving large-scale reductions in demand: netting for intraday interbank payments, changing incentives for daylight overdrafts, and changes in liquidity regulation. We also describe proposals for simple changes to open-market operations that are straightforward to implement, and for changes in the rules for interest payment on reserves, about which Fed officials are most skeptical. Without extensive further study, no one knows how much each of these would reduce the aggregate demand for reserves.

Netting mechanism for Fedwire. Duffie’s most ambitious proposal — and, alongside intraday overdraft reform, among the most promising for addressing the root cause of today’s high reserve demand — is adding a payment-netting queue to Fedwire. The Bank of England (CHAPS), the Bank of Japan (BOJ-NET), and Canada (Lynx) employ similar liquidity-saving mechanisms. Netting would allow banks to offset large outgoing payments against incoming ones before drawing on reserve balances, reducing the opening balance each bank needs to process its daily payments.

International evidence from other systems suggests reductions in required intraday liquidity in the range of 15–20 percent. But these are analogies, not predictions: Fedwire has a unique network topology, and there is no reliable estimate of how large the effect would be in the U.S. system. Importantly, in CHAPS and BOJ-NET, queued payments settle only when funds are available — the central bank never extends credit to move them through. Whether a Fedwire netting queue could work the same way or would instead require the Fed to backstop payments in the queue is a design question that any cost-benefit analysis must address.

We should caution that the operational cost of such a change to Fedwire may be enormous. Retooling the world’s largest payment system — and the internal systems of dozens of large banks — is a multi-year project. This approach is genuinely untested in the U.S. context, so its consequences for payment system resilience, bank behavior, and market functioning need careful assessment. That said, the potential is sufficient to warrant beginning the cost-benefit analysis now.

Relaxing supervisory restrictions on intraday overdrafts. The near-elimination of daylight overdraft use by large banks — from roughly $120 billion per day pre-crisis to under $5 billion today — appears to be primarily a reflection of supervisory expectations embedded in the Fed’s Comprehensive Liquidity Analysis and Review (CLAR) process and resolution planning guidance. In the current environment, banks and their supervisors treat intraday overdrafts as a signal of inadequate self-sufficient liquidity. Duffie and Miran both argue that revising these supervisory expectations could allow banks to rely more on intraday Fed credit rather than pre-loading reserves.

However, we think policymakers should be cautious here. The supervisory preference for self-sufficient liquidity exists for sound reasons. Daylight overdrafts are a form of intraday credit extended by the Federal Reserve to individual banks. If a bank fails mid-day while in receipt of an overdraft, the Fed bears the credit loss. Pre-crisis, the 10 largest banks used large overdrafts because overdrafts were a cheap source of funding that shifted credit risk to the Fed. The post-crisis supervisory tightening was a deliberate response to that experience.

Loosening supervisory expectations to reduce reserve demand would shift liquidity risk back toward the Fed. Before doing so, it is important to understand both the magnitude of the resulting risk that the Fed would bear and whether it is possible to manage the risk through collateralization and other safeguards. This is an area where the consequences of getting it wrong could be significant, and where the evidence from other financial systems may not translate cleanly to the U.S. context. Careful weighing of the costs and benefits should precede any changes.

Broadening collateral requirements for liquidity regulations. Duffie recommends two changes to Regulation YY — the Fed's enhanced prudential standards for large bank holding companies. First, allow banks to count non-HQLA (high-quality liquid asset) collateral held at Fed facilities toward the regulatory liquidity buffers. Second, reduce the supervisory preference for holding reserves — rather than Treasuries — to satisfy internal liquidity stress tests. The idea is that if banks could count a broader range of assets toward meeting their liquidity coverage ratio (LCR), they would need to hold fewer outright reserves, shifting demand inward. (Governor Miran makes similar recommendations in a co-authored working paper.)

However, once again, we encourage caution. First, Regulation YY already allows banks to incorporate discount window, SRF and FHLB advances into their liquidity stress test scenarios – but with little obvious impact on bank behavior so far. Second, there are other ways to improve liquidity during crisis episodes without relaxing collateral rules: for example, the Report of the G30 Working Group on the 2023 Banking Crisis recommends pre-positioning collateral at central banks as a way to broaden discount window access without weakening prudential standards. Finally, liquidity regulations are designed precisely so that large banks can survive a stress period without relying on the central bank. The LCR and related requirements reflect hard lessons from 2008 about what happens when banks cannot meet their obligations from their own liquid resources. Broadening the definition of eligible collateral reduces the insurance value of these requirements, potentially leaving the banking system more exposed to a liquidity crisis. Without careful study, policymakers should not assume otherwise.

Temporary open market operations (TOMOs). Duffie’s most immediately actionable (and arguably least risky) recommendation is to systematically sterilize predictable supply shocks. The biggest and easiest to anticipate shocks are quarter-end foreign-bank window dressing, Treasury General Account fluctuations, and changes to the Foreign and International Monetary Authorities’ (FIMA) reverse repo pool. Such daily Fed operations – which were standard before the 2007-09 crisis – could easily be implemented today at the FOMC’s direction. The Fed could make them more effective by using evolving tools to monitor reserve scarcity (see here).

While TOMOs would not directly reduce the structural level of reserves, they could reduce the frequency of acute shortfalls that trigger payment gridlock. This, in turn, could lower banks’ precautionary demand for reserves. Importantly, the Fed can implement TOMOs today at no regulatory cost while policymakers examine what other reforms might deliver. That makes them a good place to start.

Improving discount window and SRF accessibility. Logan reports that the Fed already is taking concrete steps to reduce the stigma of receiving funds from its facilities: Discount Window Direct for online loan requests, streamlined pledging and collateral valuation, a second daily Standing Repurchase Agreement (SRP) operation, and removal of the aggregate SRP cap. Future possibilities under discussion include central clearing of SRP operations and daily discount window auctions.

If banks become genuinely confident that they can monetize collateral posted at the Fed whenever needed, their precautionary demand for reserves should decline. At the same time, to avoid bank over-reliance on central bank funds, policymakers must decide how to price the backstop that these facilities provide: recall, for example, that Bagehot’s prescription for a penalty rate on central bank lending aimed to ensure that the central bank was the lender of last (not first) resort, and that it would be repaid first when market dysfunction receded.

Tiered reserve remuneration. Duffie proposes paying IORB only up to a “quota” of reserves each bank needs for payments, and a lower rate on holdings above that threshold. In effect, this would tax banks’ reserve holdings above the quota, reducing the return on excess reserves to below the policy rate, thereby encouraging banks to lend surplus reserves rather than hoard them. International examples (e.g., the Eurosystem, the Bank of Japan, the Norges Bank, and the Reserve Bank of New Zealand) suggest the approach can work in principle.

However, this proposal appears to have little support among current U.S. policymakers. Logan explicitly rejects tiering as “a form of central planning” that would have “drawbacks for innovation, growth and competition.” More fundamentally, introducing what is effectively a tax on bank reserve holdings could require legislation and would almost surely generate significant opposition from the banking industry. We do not expect the Fed to deploy this tool anytime soon.

How Much Can Reforms Shrink the Balance Sheet?

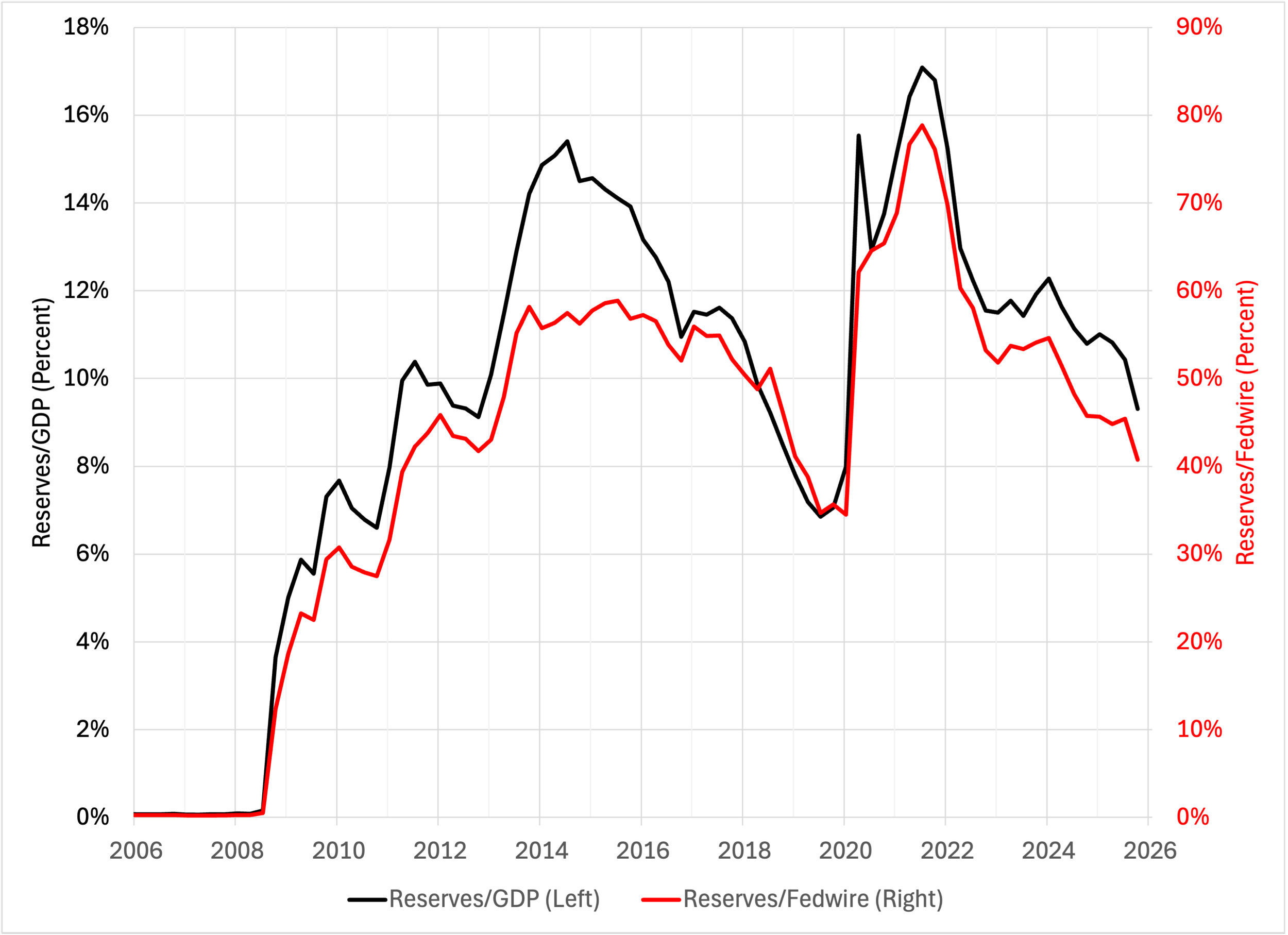

Miran's estimated reduction of $1–$2 trillion refers to total Fed assets, not reserves specifically. To achieve a large reduction of assets, the Fed would need to reduce its liabilities (which finance those assets). However, the Fed does not control the volume of key liabilities such as currency demand, foreign official deposits, or the Treasury General Account, so it would need to reduce commercial bank reserves (which it does control) virtually dollar-for-dollar with assets. In the following chart, we plot the ratios of reserves to GDP (the black line) and to average daily Fedwire volume (the red line).

Reserve Benchmark Ratios (quarterly), 2006 to 2025

Note: Fedwire volume is the sum of funds and securities. Reserves are quarterly averages of weekly data and Fedwire is quarterly averages of daily data. Source: GDP is from FRED, reserves are from the H.4.1, and Fedwire volume is from www.frbservices.org.

The working paper behind Miran's speech is more rigorous than a simple GDP-ratio exercise: it uses Monte Carlo simulations to estimate the impact of 13 policy tools and arrives at a central estimate of $1.3 trillion in reserve demand reduction. The authors themselves warn that the effects "may not be strictly additive." We would go further. The single largest contributor — a $350 billion reduction from tolerating a persistently positive EFFR-IORB spread — comes at a cost the paper acknowledges: greater money market volatility that could push precautionary reserve demand back up, partly or fully negating the very reduction it is meant to achieve. The second-largest contributor — allowing banks to count discount window capacity in their LCR — rests not on a model but on a single observed ratio: since reserves account for about one-third of banks' HQLA, the authors assume one-third of the theoretical maximum relief translates into lower reserve demand. That is an assumption, not an argument. The paper does not address the lack of observable effect from the 2024 Regulation YY guidance, which already moved in this direction.

The ultimate problem is that the $1.3 trillion estimate is not derived from a fully articulated model of equilibrium bank behavior under the proposed regulatory environment. It is a sum of partial, largely non-behavioral estimates that all depend on reduced stigma — which the paper's own analysis suggests is hard to achieve. If stigma proves persistent, the entire menu of policy options would deliver far less than suggested.

From a pragmatic perspective, the key question is not how much the balance sheet could shrink, but which reforms should come first and how we would know if they are working. On the first, TOMOs seem to be the natural starting point — low-risk, immediately deployable, and requiring no legislation or regulatory change. On the second, Logan and Duffie agree: watch the spread between SOFR and the IORB and the timing of dealer-bank payments, not the effective federal funds rate, which is too thin a market to be a reliable guide. And if the demand-reducing reforms are genuinely working, we would expect to see rising take-up at the Fed's overnight reverse repo facility — a sign that banks are shedding reserves they no longer need rather than hoarding them as a precaution.

A subtler but important fiscal point also deserves attention. Reducing reserves matched by equal reductions in Fed Treasury holdings does not cut the government's combined interest bill — and may well raise it. If the Fed supplies fewer reserves (which pay IORB) and holds correspondingly fewer Treasuries, banks will reallocate their portfolios, partly switching toTreasury securities with a longer duration than reserves. Because those Treasuries carry a higher yield than overnight reserve remuneration, the total interest cost across the consolidated government balance sheet will likely rise, not fall. Hence, the interest savings that some proponents of balance sheet reduction advertise as a benefit may be completely illusory — a point worth underscoring given Fed Chair nominee Kevin Warsh's aim to separate monetary from fiscal policy and President Trump's concerns about debt service.

What Has Changed Since February?

Our February post correctly identified the challenges of reducing the balance sheet and was right to be cautious about claims that it is simple or quick. We stand by the core structural analysis: the balance sheet cannot shrink dramatically without changing the regulatory environment and the Fed's operational toolkit. To that we now add that any major change will require significant preparation time. We also stand by our concern about sequencing — political pressure for rapid balance-sheet reduction is inconsistent with the careful, multi-year process that seems necessary.

At the same time, by focusing on payment frictions as the critical determinant for today’s high reserve demand, Duffie’s analysis points to potentially useful ways—beyond those we considered in February—for shifting reserve demand inward. The absence of netting from Fedwire and the near-total elimination of daylight overdraft use by large banks are structural gaps that deserve attention in their own right, independent of the balance sheet reduction debate.

The danger remains that political considerations – including the desire to limit Fed fiscal-like interventions outside of crises– could produce pressures for much faster reserve reductions than the current infrastructure can safely support. Proper sequencing — careful study, then staged reform, then reduction — is what makes the difference between a Fed balance sheet that shrinks safely and one that doesn't. The gauges to watch are already in plain sight. When demand for reserves naturally recedes—signaled by a narrow SOFR-IORB spread and increased reverse repo take-up—the case for shrinking supply will be far stronger.

Acknowledgement: Without implicating him, we thank our friend and colleague, Richard Berner, for his very thoughtful suggestions.