Why Private Money Needs a Central Bank

“The monetary system with the central bank at its centre has served society well. […] Private sector innovation benefits society precisely because it is built on the strong foundations of the central bank.” Bank for International Settlements, Annual Economic Report 2022, Chapter III

Money is a confidence trick. When you tap a card, swipe a phone, or send a wire, you move a claim on a commercial bank. You expect others to accept that claim at par — you send a dollar, euro, pound, or yuan, and they receive one. The claim settles and life goes on.

This apparent simplicity conceals an elaborate architecture. Commercial bank deposits circulate at par with central bank money (reserve liabilities) because a complex legal and institutional framework makes the parity credible. Prudential regulation constrains bank risk-taking. Supervision enforces the constraints. Deposit insurance reduces the incentive to run (or to panic). The lender of last resort keeps solvent banks liquid when private funding evaporates. Settlement in central bank money anchors the payment system. Each element reinforces the others. Start stripping them away and private liabilities like bank deposits will stop functioning as money.

Stablecoin advocates ignore these essential foundations. They point to asset backing — in some cases, with quality determined by legislation like the GENIUS Act — and a programmable ledger, and stop there. That is not enough. General acceptance of private money — digital or otherwise — depends on functions that only a central bank can provide. Tokenized deposits inherit this institutional support; stablecoins do not. That is why tokenized deposits will likely dominate stablecoins outside the crypto ecosystem (see here), and why the GENIUS Act distinguishes between bank-affiliated and non-bank issuers: this is the traditional, widely tested architecture.

The three properties of money

Money gains general acceptance through three properties: monetary uniformity, transferability, and elasticity (for a closely related framework, see the BIS 2025 Annual Economic Report). These properties seem obvious only because modern monetary systems deliver them reliably. That was not the case before the advent of central banks.

Monetary uniformity means one dollar trades for another dollar, regardless of who issued it. A dollar at one U.S. bank equals a dollar at another U.S. bank equals a dollar bill issued by the Federal Reserve, and they all trade at par value to the unit of account. In contrast, during the Free Banking Era (1837-1863), there were thousands of competing bank notes that traded at shifting discounts depending on the issuer, the distance to the issuing bank, and the latest news about solvency (see here). Monetary uniformity rests on convertibility — the promise that a depositor can readily exchange a bank deposit for cash under all conditions on demand and at par.

Transferability means claims move easily between users and across institutions, at low cost and at any time. Speed alone is not enough. Transferability requires that every payment end in final settlement — yielding a credible claim that is free of private credit risk. Only public money — such as cash or central bank reserves — can make that endpoint final. Final settlement is what lets a dollar move from one holder to another without either side worrying about the other’s failure.

Elasticity means the quantity of money expands and contracts with demand. In good times, banks create deposits as they extend credit. In times of stress, demand for safe liquid assets spikes. Unless the quantity of money can expand during a panic, deflation and gridlock follow. Elasticity requires a backstop that expands the quantity of money on short notice when private issuers cannot.

How does a central bank make private money possible?

Each of the three properties of money depends on the central bank.

Monetary uniformity requires a lender of last resort. You might think that a well-capitalized bank with a prudent balance sheet can always honor redemptions so convertibility at par relies on holding enough safe assets to back deposits. This description applies to a “narrow bank” that backs all deposits with central bank reserves.

But banks today are not “narrow”: they issue short-term liquid deposits to finance long-term illiquid loans. No share of safe reserves short of 100 percent closes the gap between the two. If all depositors ask for their money at once, the bank cannot pay them. Some loans may not come due for years. The lender of last resort exists precisely because no bank can survive a run on its own. Bagehot's 1873 prescription — lend freely, against good collateral, at a penalty rate — has held up for more than 150 years because the problem it addresses has no private solution. Deposit insurance addresses the same fundamental problem (see Diamond). But coverage is incomplete, so uninsured depositors still run (see here).

Transferability at scale requires settlement finality in central bank money. Fedwire, the Federal Reserve's real-time gross settlement system, settles the majority of large-value interbank dollar payments in the United States. CHIPS, operated by The Clearing House, settles the rest — but net balances on CHIPS ultimately settle on Fedwire at the end of each day. Private settlement creates a credit exposure between the parties and the institution that clears them. Central bank settlement eliminates it. Reserves move and the payment is final. No participant bears the risk of another’s failure. Confidence in this finality is what allows Bank A and Bank B to treat each other's deposits as interchangeable.

Elasticity requires that private money creation can continue through all conditions, including stress. Only central bank backing makes that possible. No private issuer can manufacture reserves during a panic. No private arrangement has the unlimited resources needed to make a credible commitment to lend against illiquid collateral when funding markets close. The central bank does. This is not a subtle point. It is the primary reason why Congress created the Federal Reserve System in 1913 — to provide liquidity to solvent banks facing a panic.

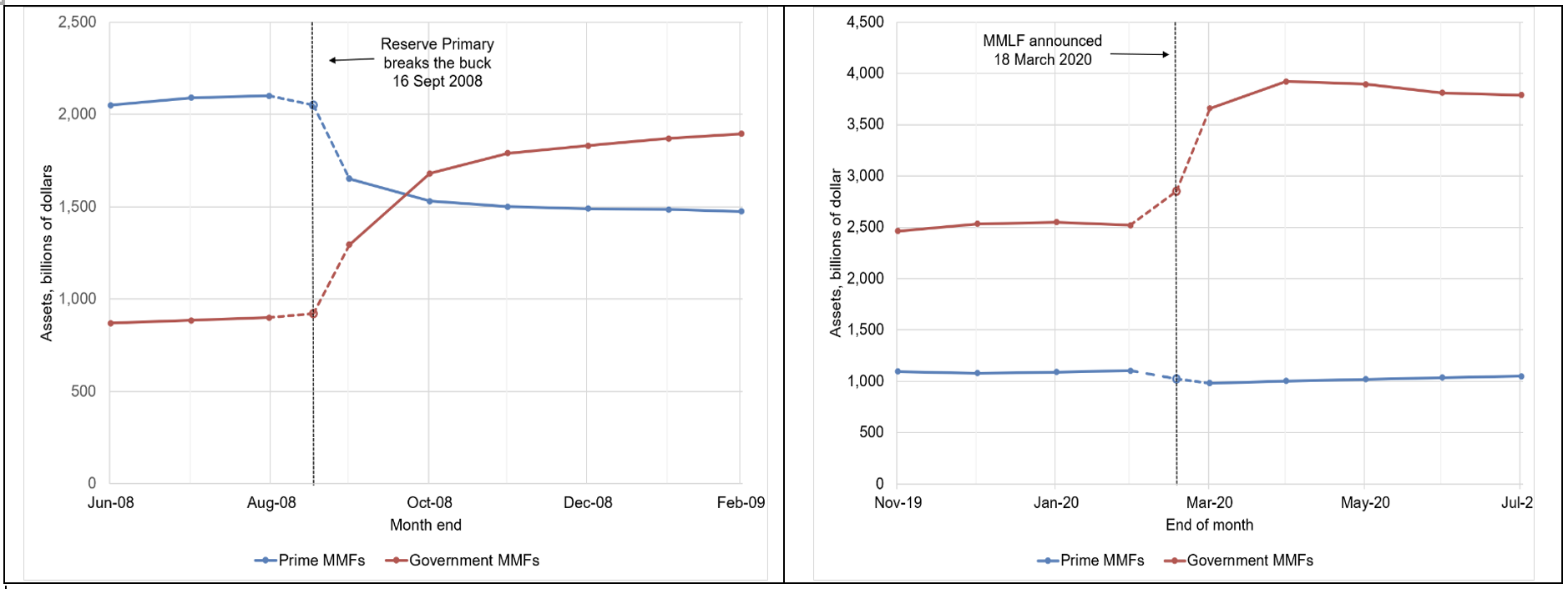

Money market funds (MMFs) illustrate how the three properties fail together, making the funds vulnerable to runs and panics. MMFs issue shares that promise redemption at par on demand and hold short-term, high-quality assets — commercial paper, Treasury bills, certificates of deposit. Their shares usually function as money-like claims: investors treat them as cash equivalents.

But MMF issuers have no central bank account, no deposit insurance, and no standing access to central bank credit. When confidence in par convertibility collapses, only emergency government action can stop a panic. In September 2008, the Reserve Primary Fund — a prime money market fund — broke the buck after the Lehman bankruptcy and prime MMFs across the industry suddenly faced a wave of withdrawals. Within days, the Treasury guaranteed MMF shares and the Fed created emergency lending programs to finance bank purchases of MMF assets. In March 2020, a similar panic led the Fed to create new lending programs to do essentially the same thing (see our discussions here and here).

Both episodes showed what happens when a private money-like claim faces a run without standing access to a central bank backstop. Monetary uniformity failed first: Reserve Primary broke the buck, and par convertibility collapsed across prime MMFs. Transferability failed next, as counterparties refused to accept MMF shares at face value. Elasticity failed last: as investors fled, the quantity of money-like claims contracted precisely when the economy needed it to expand. Treasury intervention helped, but only the Federal Reserve could restore all three properties at once. (For in-depth analyses of the role of central banks in making money reliable, see Barcelona 8: Digital Money.)

The figure below shows the pattern. In both episodes, investors fled from prime MMFs to government MMFs — from funds holding private claims to funds holding public ones. In 2020, the investors also fled from uninsured deposits. As a result, government MMFs absorbed more than a trillion dollars of new inflows as investors sought the safest short-term claims they could find. Federal Reserve lending programs made this sudden migration orderly rather than catastrophic (see here).

Money Market Fund Assets Around the 2008 (left panel) and 2020 (right panel) Runs (Billions of Dollars)

Note: Monthly data understate the intensity of the March 2020 run: prime institutional MMFs lost roughly $125 billion in the week before 18 March, when the Federal Reserve announced the Money Market Mutual Fund Liquidity Facility (MMLF). Sources. Investment Company Institute (ICI) Money Market Fund Assets (month-end values). Values for 16 September 2008 and 18 March 2020 are authors' estimates. In both cases, we anchor the event-date values around the available month-end data. Based on a variety of other sources, we attribute roughly one-third of the February-to-March 2020 flow to the period through 18 March.

Tokenized deposits inherit the foundation. Stablecoins do not.

The logic that applies to traditional money-like instruments also applies to privately issued digital liabilities. Whether they function as money depends on the institutional framework that supports them. Technology can change how claims move and settle, but it does not alter what stands behind them.

Tokenized deposits and stablecoins illustrate the difference. A tokenized deposit is a claim on a supervised bank. It therefore sits inside the institutional framework that makes private money generally accepted — access to the lender of last resort, deposit insurance, and participation in the payment system that ultimately settles in central bank reserves. Tokenization changes how the deposit moves — 24/7/365 settlement on a programmable ledger — but the institutional position does not change. A tokenized deposit is still a deposit.

Stablecoins lie outside the perimeter protected by the central bank. A fiat-backed stablecoin promises redemption at par, but a nonbank U.S. issuer lacks the central bank backing to make this promise credible. To defend its redemption commitment, the issuer holds short-term financial assets, such as Treasuries, bank deposits, or money market fund shares. Yet, if the issuer faced a surge of redemptions — as MMFs did in 2008 and 2020 — it would have to liquidate these assets into a falling market. That is a recipe for breaking the buck.

The GENIUS Act effectively acknowledges that private money requires central bank backing. It channels bank-affiliated issuers into the existing banking regulatory perimeter, where their parent institutions already have full master accounts and access to central bank credit (including intraday overdrafts and discount window access). It creates a separate federal license, supervised by the OCC, for non-bank issuers but leaves their eligibility for Federal Reserve services to existing law. In practice, non-bank stablecoin issuers cannot draw on central bank credit — or even earn interest on central bank deposits — without a change in Fed policy. In contrast, bank-affiliated stablecoins can tap the infrastructure through their parent institution.

Unlike the United States, the United Kingdom would blur the boundary between major stablecoin issuers and banks. The Bank of England's proposed regime grants systemically important sterling stablecoin issuers access to U.K. payment systems and contemplates emergency lending against high-quality collateral — extending lender-of-last-resort access to systemic stablecoins. To manage the resulting risk, the Bank of England would regulate systemic nonbank issuers as banks — applying prescriptive reserve requirements, capital requirements, holding caps, and redemption rules.

The European Union (EU) framework differs markedly from both the U.S. and U.K. versions. Under MiCA, the EU extends no backing to stablecoin issuers — bank or nonbank. Instead, it imposes constraints designed to keep stablecoins small.

Despite these stark differences, all three frameworks answer the big question in the same way: a private liability cannot function at scale without the central bank.

Why this matters for the policy debate

The stablecoin debate often proceeds as if technology were the decisive variable. It is not (see our August 2025 post). Tokenization and programmability are real advances. But these capabilities operate on top of the institutional framework that makes a claim function as money. They do not create such a framework. No ledger, no matter how efficient, can deliver monetary uniformity under stress, final settlement in public money, or elasticity during a panic. Those properties come from institutions, not from code or the structure of the ledger. Any stablecoin that aspires to function as general-purpose money will eventually need access to the same central bank support that stands behind bank deposits. When that happens — and the Bank of England proposes it openly — the stablecoin becomes, in substance, a regulated bank liability.

This assessment leads us to reframe several active questions.

Should stablecoin issuers get full Fed master accounts? Our answer: only if they accept bank-equivalent regulation and supervision (see our June 2021 post). Recent proposals for granting legally eligible institutions “skinny” master accounts at the Fed typically cap the account size and exclude access to Fed credit and to interest on reserve balances (see, for example, Waller). The question is whether the Fed can credibly refuse to provide credit to these clients in a crisis: if they cannot — as proved to be the case in the 2008 and 2020 MMF episodes — then these payment accounts are not sufficiently skinny.

Will non-bank stablecoins scale into mainstream payments? We strongly doubt it. They lack the institutional foundation, while the GENIUS Act appears to foreclose the path to acquiring it.

Will tokenized deposits dominate stablecoins outside the crypto ecosystem? Yes, and the reason is not technology. It is primarily because tokenized deposits are already inside the institutional perimeter that makes private money work.

Ultimately, the future of digital money will turn less on technology than on whether the central bank stands behind it. Settlement finality, lending of last resort, and the backing that sustains private money creation under stress — these are the functions no private arrangement can fully replicate. Private liabilities backed by the central bank will circulate as mainstream money. Private liabilities without that backing will not.